Peak Token: Why the Frontier Just Priced Itself Out of Its Own Market

Jensen said spend $250k/year per engineer on tokens. The world heard him—then saw the bill. Open-source models match the frontier for a fraction of the cost. The model makers are going public the same month their pricing power runs out.

Stephen Messer, Co-founder of Collective[i] and LinkShare (sold to Rakuten for $425M, 1996–2005). Entrepreneur of the Year. Board member, Spire Global (NYSE: SPIR). Building intelligence.com

At GTC 2026, Jensen Huang sat down on the All-In Podcast and made the statement of the year for the AI industry, possibly without realizing what he was setting in motion. Asked whether Nvidia spends $2 billion a year on tokens for its own engineering team, Jensen answered, “We’re trying to.” He went further. If an engineer earning $500,000 a year was not consuming roughly $250,000 in tokens, he said he would be “deeply concerned.” If they had spent only $5,000 by year-end, he would “go ape.”

It was the kind of thing only Jensen could say, in the leather jacket, with the conviction of a CEO who sells the picks and shovels and would obviously prefer the gold rush to last another decade. He framed it as productivity. Engineers who use AI sparingly are like chip designers reaching for paper and pencil. The framing landed. The number lodged in every CTO’s head. And within weeks, the entire industry had a new metric: tokens consumed per employee.

Meta built a leaderboard. They called it Claudeonomics, named after the Anthropic models burning at the top. The dashboard ranked all 85,000 Meta employees by token usage, awarded titles like “Token Legend” and “Cache Wizard,” and surfaced the top 250 power users. In thirty days, Meta employees burned 60.2 trillion AI tokens. Two days after the leaderboard went public, Meta took it down. The reason given was data leakage. The real reason, according to the engineers who watched it play out, was that the work being done at the top of the leaderboard was nonsense. People were running pointless tasks to climb the rankings, because the rankings were what got noticed.

Amazon ran the same play with a tool called KiroRank. They killed it in October 2024, after employees figured out they could inflate their scores by assigning AI tools throwaway work and watching their numbers climb. The token spend on the leaderboard was real. The value created by it was not.

Salesforce went the other direction and made tokenmaxxing official policy. A Mac widget that updates every fifteen minutes, showing each engineer their own spend and a minimum expected number. Last week’s targets were $100 on Claude Code and $70 on Cursor. The engineers I have spoken with describe it the way prisoners describe an exercise routine: you do it, and you find ways to do it that look productive, and you do not ask questions about whether any of it matters.

This is what happens when a leader of Jensen’s stature names a metric. Companies optimize for the metric. The number Jensen wanted to go up went up. The value that was supposed to ride along with it did not.

Meta burned 60.2 trillion tokens in 30 days, and the people at the top of the leaderboard were doing throwaway work to stay there. Salesforce mandated minimum daily spend per engineer. The number Jensen wanted to go up went up. The value that was supposed to ride along with it did not.

Goodhart’s Law Comes for AI

There is a principle in economics called Goodhart’s Law. When a measure becomes a target, it ceases to be a good measure. The moment leadership picks a number and ties incentives to it, the organization stops producing the underlying thing the number was supposed to represent and starts producing the number directly.

This is not a new mistake. McNamara measured the Vietnam War in enemy body counts. The body counts went up. The war did not get closer to winning. Wells Fargo measured new account openings. The account openings went up. They were fake. Every generation gets a fresh version of the same lesson, and every generation believes its number is different.

Token consumption is the current version. It was easy to measure, easy to compare, easy to put in a slide. It came from the most credible voice in the AI industry. And it correlated, briefly, with the experience of using AI well. Engineers who used AI heavily early on did get more done. The correlation made the causation feel obvious. It was not.

Uber is the cautionary tale already on record. The company spent eight figures on internal AI tooling in 2024 and 2025, much of it concentrated on enabling engineering and operations teams to burn through tokens at frontier model prices. The token consumption looked impressive on dashboards. The P&L impact was almost nothing. An MIT NANDA study published in 2025 found that 95 percent of enterprises deploying AI saw zero measurable financial benefit, despite collectively spending tens of billions. The other 5 percent were not spending more on tokens. They were spending differently. The gap between the winners and the rest is structural, not budgetary.

The tokenmaxxing pattern is the AI version of the same trap every organization eventually falls into. Pick the wrong metric, optimize the wrong behavior, mistake activity for outcome. The companies that figured this out first are already doing something different. The companies still building leaderboards are about to learn it the expensive way.

The Frontier Just Lost Its Moat

The second thing that happened while Jensen was telling the world to spend more on tokens is that the price of those tokens was collapsing for anyone willing to look past the frontier brand.

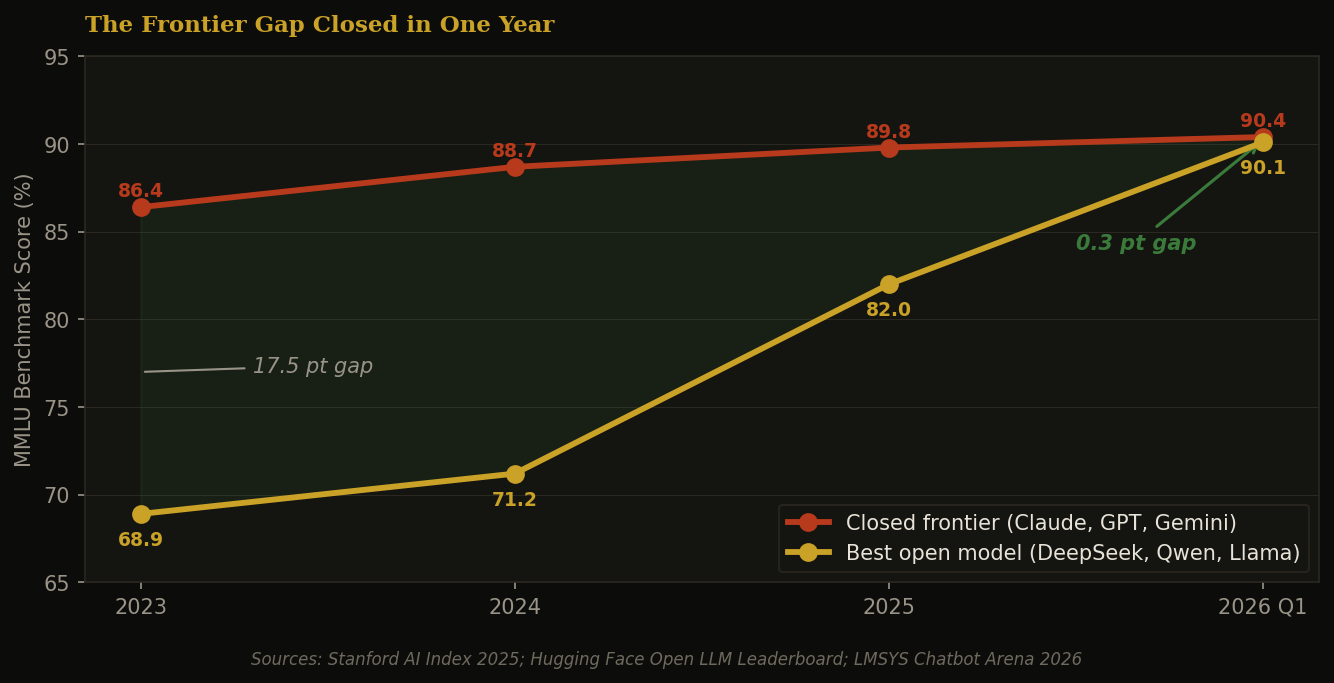

For three years, the case for paying $15 per million tokens for Claude Opus or $10 for GPT was straightforward. The frontier was meaningfully smarter than anything else available. That gap justified the price. In 2024, the difference between the best closed model and the best open model on MMLU was 17.5 percentage points, the kind of margin that makes the cost decision easy. You pay for the frontier because the frontier delivers measurably better results.

That argument no longer holds.

The gap between the top closed model and the top open model on MMLU closed from 17.5 points in 2023 to 0.3 points by Q1 2026. Five independent open families reached frontier quality at roughly the same time. Sources: Stanford AI Index 2025; Hugging Face Open LLM Leaderboard; LMSYS Chatbot Arena 2026.

The gap is now 0.3 points. The capability premium that justified the frontier price is statistically indistinguishable from zero on most benchmarks, and what remains is concentrated in a few narrow areas like production coding and complex agentic tasks. For the bulk of what enterprises actually use AI for, the open-source models are at parity. And the price difference is not subtle.

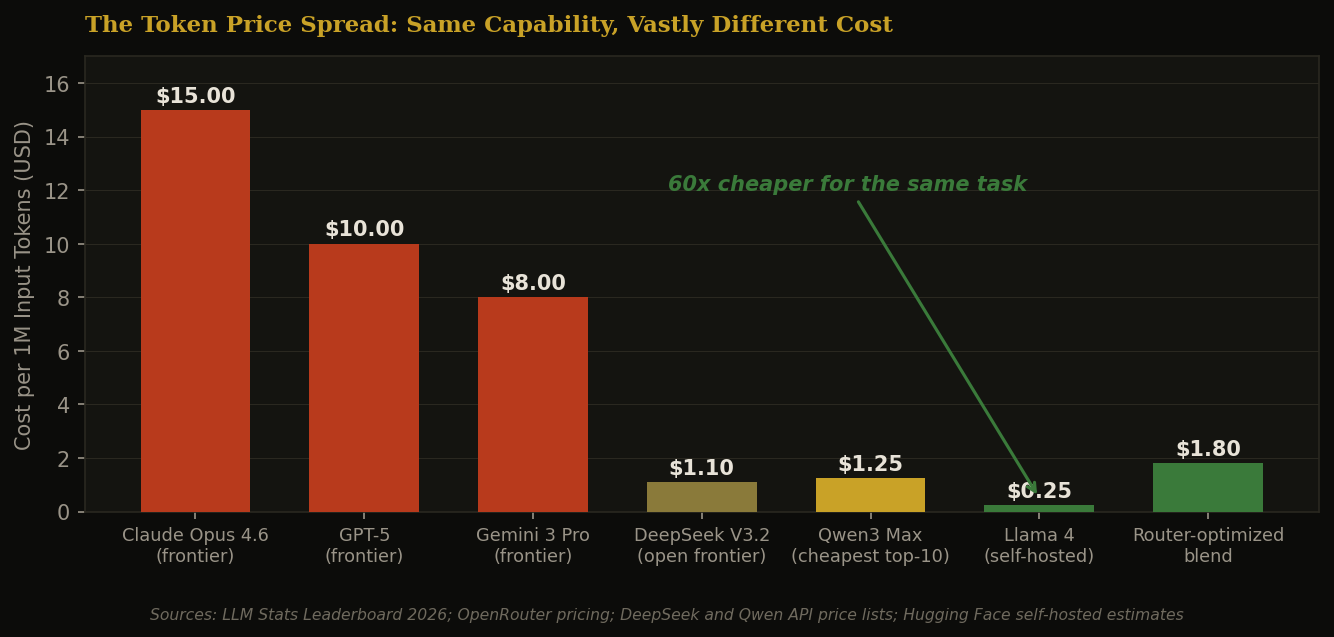

The token price spread across capable models is now roughly 60x. The frontier brands sit at the top. The open-source frontier and self-hosted options sit at the bottom. A router that picks the right model per task can blend the two. Sources: LLM Stats Leaderboard 2026; OpenRouter; DeepSeek and Qwen price lists.

DeepSeek V3.2 runs at roughly $1.10 per million input tokens, down from frontier prices that were 10 to 15 times higher a year earlier. Qwen3 Max sits at $1.25, the cheapest in the top ten by benchmark performance. Llama 4, if you self-host it, drops the marginal token cost to a fraction of that. The 60x spread between the most expensive frontier token and the cheapest capable open token is not a market inefficiency. It is the new shape of the market, and the buyers have noticed.

This is what makes Jensen’s $250,000-per-engineer recommendation read very differently in retrospect. He may have helped trigger peak token spend exactly as cheaper alternatives became indistinguishable in quality. The leaders who spent the most aggressively in 2025 and early 2026 are now sitting on contracts they would not sign again, with frontier providers whose pricing power is eroding by the quarter. The leaders who waited, or who built more flexibly, are the ones positioned to actually capture the savings.

The Routing Layer Becomes the New Stack

A 60x price spread does not stay in a market for long without someone arbitraging it. The companies that have figured out how to route the right model to the right task at the right moment are now the most interesting infrastructure layer in the AI stack.

OpenRouter started as a simple proxy: one API across hundreds of models. It has become something more like an intelligence layer that picks the cheapest model capable of handling each query. Martian, NotDiamond, and a wave of similar companies built their products around the same insight. Send the simple queries to the cheap model. Send the hard queries to the frontier model. Most queries are simple. The blended bill drops 70 to 85 percent without measurable quality loss, according to research from UC Berkeley and Canva on intelligent routing.

Rob May, who founded Backupify and now runs HalfCourt Ventures, co-founded Neurometric.ai in January 2025 to attack the same problem from a different angle. Neurometric’s pitch to Fortune 1000 enterprises is task-based routing: identify the highest-volume workloads, train small specialized models for each, and reserve frontier models for the genuine reasoning problems. Rob describes the typical customer arc bluntly. A company is spending $200,000 per month on frontier-model inference, growing 40 percent month over month, with no end in sight. They identify the top workload, often something like customer sentiment analysis at $32,000 per month. They route it to a small specialized model. The bill collapses for that workload. Then they do it again for the next workload. The frontier model use does not go to zero. It goes to where the frontier model is actually needed, which turns out to be much narrower than anyone first assumed.

This is the architecture leaders should be building toward. Frontier models for the genuinely hard problems. Open-source models for the common ones. Small specialized models for the high-volume repetitive ones. A router that picks the right model per task, automatically. And underneath it all, harnesses like Hermes and the OpenClaw projects that abstract the model layer entirely, so the application does not know or care which model is serving the request.

The harnesses matter more than they look. They are the layer that decouples the work from the provider. Once your agentic stack runs through a harness, swapping Claude for Gemini for DeepSeek is a configuration change, not a rewrite. The lock-in that Anthropic and OpenAI have spent years building, the Claude Code workflows and the OpenAI Assistants ecosystem, evaporates the moment the harness layer becomes standard. And the harness layer is becoming standard faster than the frontier labs would like.

The harness layer decouples the work from the provider. Once your stack runs through a harness, swapping Claude for Gemini for DeepSeek is a configuration change. The lock-in that the frontier labs have spent years building evaporates the moment the harness layer becomes standard.

The Edge Just Caught Up

There is one more shift happening at the same time, and it is the one most enterprises have not priced into their thinking yet. The compute is moving to the device.

Microsoft’s Copilot+ PC specification, which requires a 40 TOPS neural processing unit, was originally a marketing exercise. By Build 2026, it had become something different. Microsoft retired the rigid hardware certification and replaced it with a tiered model that scales AI workloads across NPU, CPU, and GPU on the same machine. The Windows AI Platform now ships with over 40 local models accessible through standardized APIs. DirectML 2.0 abstracts away the silicon differences between Intel, AMD, Qualcomm, and the new Nvidia ARM chips. A developer writes one AI application and it runs on every NPU-equipped Windows machine.

The procurement agent Microsoft demonstrated at Build read email attachments, cross-referenced a local SQLite database, updated a Teams tab, and generated a draft contract. All on a Dell laptop. Offline. No tokens billed.

For workloads that fit on the device, the marginal cost of inference just went to zero. The privacy story improved at the same time, because the data never left the laptop. For an enterprise running an agentic workflow against sensitive data, this changes the entire procurement calculation. A small specialized model that runs locally on a Copilot+ PC, orchestrated through a harness that knows when to escalate to the cloud, is dramatically cheaper than the equivalent workload sent entirely to a frontier API. And for many workloads, including most internal coordination tasks, the local model is sufficient on quality.

This is the convergence that makes the next eighteen months interesting. Open-source models at frontier quality. A 60x price spread between the cheapest capable model and the most expensive. Routing layers that arbitrage the spread automatically. Harnesses that abstract the provider entirely. And new hardware that runs capable models locally at marginal cost approaching zero.

The leaders who understood this early built differently from the start. They never put their entire workload on one provider. They instrumented their AI architecture to measure cost per outcome, not tokens consumed. They invested in the routing and harness layers as core infrastructure, not afterthoughts. The leaders who optimized for tokenmaxxing are now looking at contracts that lock them into the most expensive supplier for capability they can get elsewhere for a tenth of the price.

What This Means for the IPOs

Now look at the calendar. Anthropic filed confidentially in late May 2026 at a $960 billion valuation. OpenAI followed in early June, targeting roughly $1 trillion. Both companies are going public the same year token prices are collapsing, open-source quality has reached parity, and the customers they need to keep are actively building architectures designed to use less of their product.

This is the question every public investor will eventually have to answer.

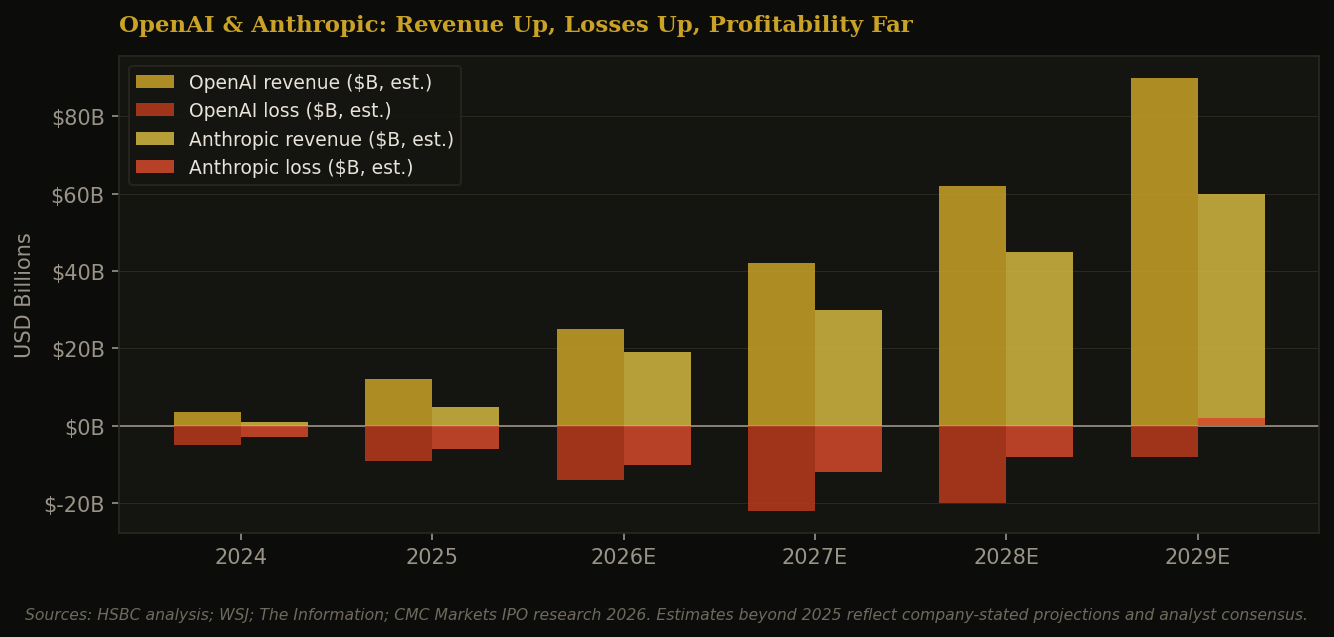

OpenAI projects $25B in 2026 revenue and $14B in losses, with profitability not expected until 2029 or 2030. Anthropic crossed $30B annualized revenue with planned 2026 infrastructure spending near $19B. Both grow fast. Neither has shown a path to profit that does not require token prices to hold. Sources: HSBC; WSJ; The Information; CMC Markets 2026.

I covered the structural case against the model makers in The Bear Case for the Model Makers. The valuation math is the same here, viewed from the customer rather than the capital structure. OpenAI is asking the public market to pay 40 times revenue for a business that loses $14 billion this year and does not expect to be profitable until 2029. Anthropic is asking for similar multiples on a similar trajectory. Both numbers price in continued pricing power, frontier dominance, and customer growth that compounds.

Every assumption underneath those multiples got weaker in the last six months. Pricing power is eroding because the alternatives are good enough. Frontier dominance is eroding because the open-source frontier is now 0.3 points behind on benchmarks. Customer growth is real, but the customers themselves are quietly architecting around the assumption that frontier model spend is the expensive part of their AI bill they need to engineer away.

The IPO question is not whether OpenAI and Anthropic are remarkable companies. They are. The question is whether the valuations price the Microsoft outcome or the Google outcome. Microsoft trades at 12x sales because it owns the operating system layer and the productivity suite and the cloud. Google trades at 6x sales because the underlying product became a commodity and the company makes its money on the advertising layer above it. OpenAI at $1 trillion against $25 billion of revenue is pricing the Microsoft outcome. The structural evidence available right now points to the Google outcome.

This is what makes the timing so peculiar. The IPOs are arriving exactly as the moat that justified the valuations is closing. The buyers underwriting the public offerings are pricing a market position that no longer holds the way it held when the deals were structured. The companies are not bad. The price might be.

The Architecture Leaders Should Be Building

For the leaders thinking about this from inside an enterprise rather than from a portfolio manager’s desk, the implications are practical and immediate.

Stop measuring tokens. The metric that mattered in 2024 is the metric that misleads in 2026. Measure cost per outcome. Cost per resolved support ticket. Cost per closed deal. Cost per shipped feature. The question is not how many tokens your team burned. The question is what business result those tokens produced and what it cost.

This is the lens we build through at Collective[i]. The agents we ship surface insights from our economic models, the patterns in sales, business development, and M&A that no single company can see from its own data, and our clients evaluate every one of those insights through the same question: what is the return. An insight that helps close a deal, find an acquisition, or open a market is worth a multiple of what the agent that produced it costs to run. We hold ourselves to that arbitrage. The value a client gets has to be a large multiple of what they pay, which is exactly why we can charge less and still build a durable business. Start with the value to the client, make the math obviously work in their favor, and the rest follows. A token metric measures our cost. An ROI metric measures their gain. Only one of those is worth optimizing.

Architect for substitution from day one. Every workload should run through a routing layer or a harness that can swap models without rewriting the application. The cost of building this once is small. The cost of not building it is being locked into the most expensive supplier exactly when the cheapest capable supplier becomes good enough. All AI is narrow intelligence. Running one model for everything is the wrong architecture by definition. Running the right model for each task is the architecture that actually wins.

Move what you can to the edge. The Copilot+ generation of devices changes the math for any workload involving private data, predictable patterns, or latency sensitivity. A small specialized model running on a laptop with a harness that escalates to the cloud only when needed is the cheapest capable architecture for most enterprise agentic workflows. Build for it now.

Pick infrastructure over models. The harness layer, the router, the orchestration framework, the observability stack: these are durable assets that outlive any specific model. Pick model providers carefully. Pick infrastructure choices like you mean to keep them.

The leaders who do this will spend less and learn more. The leaders who continue to chase tokenmaxxing will spend more and learn that they paid for the wrong thing. The frontier model makers will continue to do important research and produce capable systems. They will probably not be priced the way they are priced today five years from now. The market does not stay 60 times spread on a commodity, and the frontier is now close enough to a commodity that the spread is the story.

Jensen will get his $1 trillion of compute demand. He was right about that. He may have helped the demand peak earlier than his shareholders would have preferred, by giving the world a vivid number to optimize toward and triggering the architectural response that is now collapsing the price of the thing he was selling. That is the strange thing about credible CEOs naming metrics. The number goes up. The market adjusts. And the company that wins next is the one that read the adjustment correctly the moment the metric stopped meaning what it used to.