Software Is Over

Don’t let it be the anchor that pulls your company under. 30 years at the intersection of tech and disruption: LinkShare before affiliate marketing, Spire Global before satellite data, Collective[i] before AI. Every disruption follows the same shape. Here’s what this one requires.

Stephen Messer, Co-founder of Collective[i] and LinkShare (sold to Rakuten for $425M, 1996–2005). Entrepreneur of the Year. Board member, Spire Global (NYSE: SPIR). Building intelligence.com

Eight days ago, Salesforce co-founder Parker Harris stood on stage at their developer conference and asked: “Why should you ever log into Salesforce again?” He was announcing Headless 360, which makes the entire Salesforce platform accessible without a browser, operated entirely by agents. He mentioned that Salesforce had been building it for two and a half years. That means they started building the architectural replacement for Agentforce before Agentforce publicly launched. They shipped the product. Sold the contracts. Built the replacement simultaneously. He was announcing the end of his own company’s business model. And he was right.

Software is over.

Not as infrastructure. Your Salesforce contract doesn’t expire tomorrow. But as the primary organizing logic for how technology creates competitive advantage, it’s done. The companies that understand why will have a compounding head start over the ones still optimizing around the old logic.

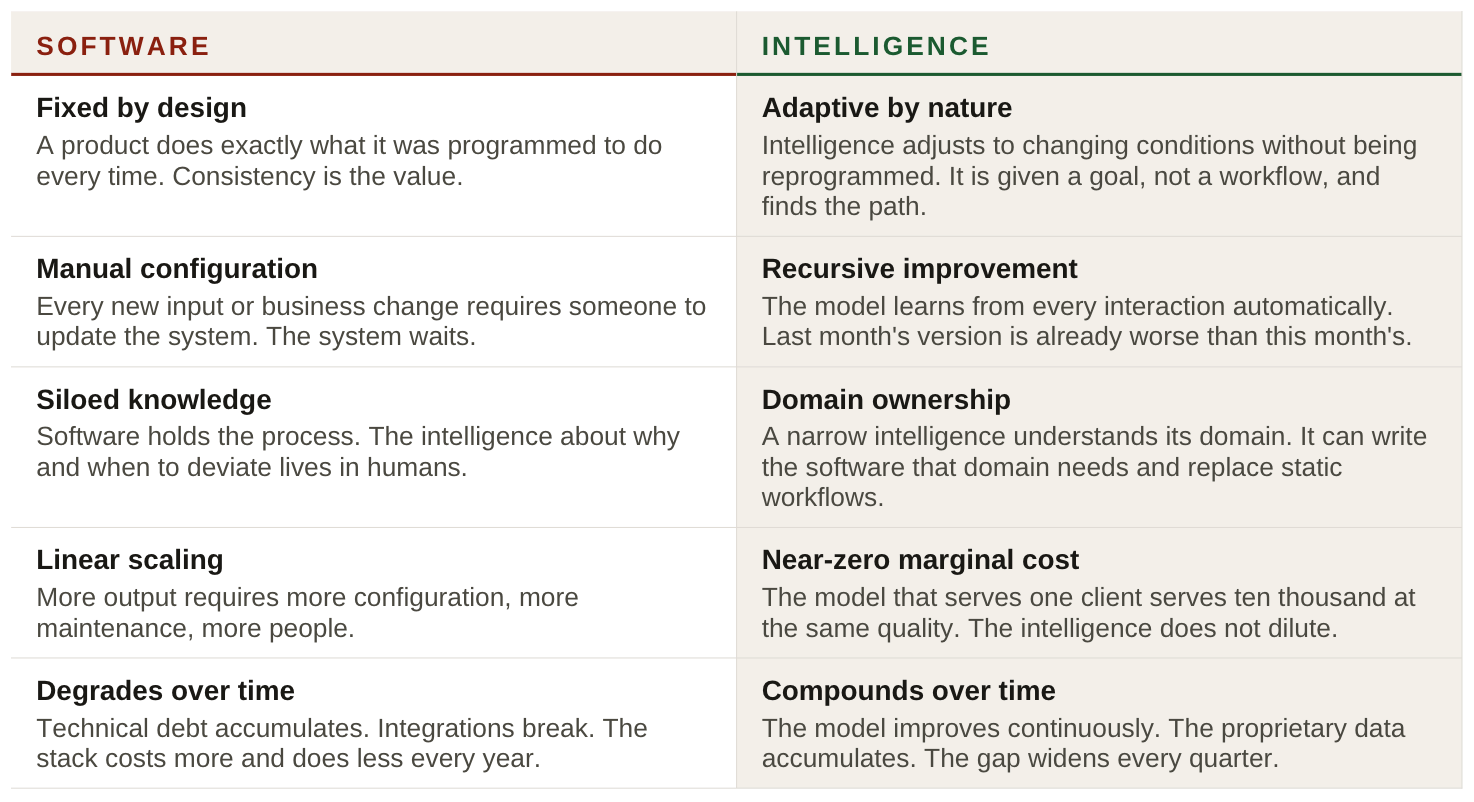

Intelligence is not a feature. It's the new substrate.

Every major technological era has had a substrate, the foundational layer everything else runs on. The industrial era ran on electricity. The information era ran on software. Both transitions followed the same pattern: the new substrate didn’t improve what existed, it replaced the logic underneath it. You didn’t bolt electricity onto steam engines. You redesigned the machine.

Intelligence is the new substrate. Not a feature you add to software. Not an AI layer on top of your CRM. The thing that everything else will run on. And it behaves categorically differently from software.

The reason this matters: software companies built their entire business model around the opposite of these properties. SaaS recurring revenue depends on switching costs, integration lock-in, and the friction of change. Intelligence has none of these natural moats, unless the intelligence itself is the moat, because the data that trains it is proprietary and the network that feeds it is irreplaceable.

Your software stack is the blocker, not the foundation.

The average enterprise runs between 130 and 900 SaaS applications. Each one was bought to manage a specific process. Each one was integrated with two or three others. Each integration was a custom project. Each integration breaks when either system updates. Each broken integration requires a human to notice, diagnose, and fix it.

This is not mismanagement. It is what happens when the correct answer, buying the best tool for each job, integrating them, managing the stack, gets applied consistently for twenty-five years. The software stack that made your company efficient in 2005 is the infrastructure that makes your AI transformation slow in 2026.

AI agents need context. To plan, to decide, to execute, they need to see what’s happening across your CRM and your ERP and your support system and your finance platform simultaneously. The current stack makes this structurally impossible because the data is locked in silos that were designed to be independent.

The companies winning with intelligence are not connecting more tools. They are removing tools and replacing them with models that own the domain entirely. The software stack is not the foundation of their AI strategy. It is the thing being replaced by it.

Software is the most expensive thing your company owns that isn’t producing intelligence. Every dollar you spend maintaining the stack is a dollar not building the thing that will eventually make the stack unnecessary.

The market already knows: the valuation collapse in the signal

The stock market is not always right. But it is almost always early. And right now it is pricing in the end of software as a growth engine with considerable precision.

In 2025, while the S&P 500 rose 17.6%, the SaaS index fell 6.5%. The median SaaS revenue multiple, which peaked at 18x in early 2021, sits at roughly 3x today. That is not a correction. That is a repricing of the category’s future.

The intelligence companies are moving in the opposite direction at a speed that has no precedent in enterprise technology. Anthropic went from $1 billion in annualized revenue in January 2025 to $30 billion by April 2026. Fifteen months. Salesforce took twenty years to reach the same scale. OpenAI went from $6 billion ARR in 2024 to $24 billion run-rate in April 2026, tripling for two consecutive years. Meritech’s Alex Clayton reviewed the IPO trajectories of over 200 public software companies and said he had never seen a growth rate like this.

When Anthropic published a blog post about using Claude Code to modernize COBOL, the programming language that runs IBM’s mainframe business, IBM shares dropped 13.2% in a single day. Their worst single-session decline since October 2000. When Cowork launched, ServiceNow, Salesforce, Snowflake, Intuit, and Thomson Reuters all fell sharply. The market is not waiting for case studies. It is already repricing every software company that cannot answer the question: what happens to our revenue when intelligence covers our domain?

The model layer eats everything

On April 13th, 2026, Lovable, a startup that went from $1M to $200M ARR in twelve months and raised $330M at a $6.6 billion valuation, launched their payments product, positioning it as their business model moat. The day before, leaked screenshots circulated showing a full-stack app builder integrated natively into Claude, the AI that Lovable runs entirely on. No Lovable subscription needed.

This is not a story about Lovable making mistakes. Their product was genuinely good. The architecture was the problem. Lovable built the distribution layer, the UX, and the workflow on top of Anthropic’s intelligence layer. The moment Anthropic decided to serve non-technical builders directly, the premise of Lovable’s business changed overnight.

The platform eats its best clients. Every time. Salesforce killed the ISVs that got too big. Apple killed the apps it could build natively. The pattern is decades old. The speed is new. What used to take a decade now takes eighteen months.

Intelligence doesn’t just replace interfaces. It can write the software it needs, maintain it, and improve it, for a fraction of what the software cost before. Every narrow intelligence layer: language, code, images, economics. Each owns its domain completely. Jasper raised $131 million at a $1.5 billion valuation, hit $120 million in revenue, and watched it collapse to $55 million in a single year when ChatGPT shipped a better interface. The wrapper died the moment the model improved.

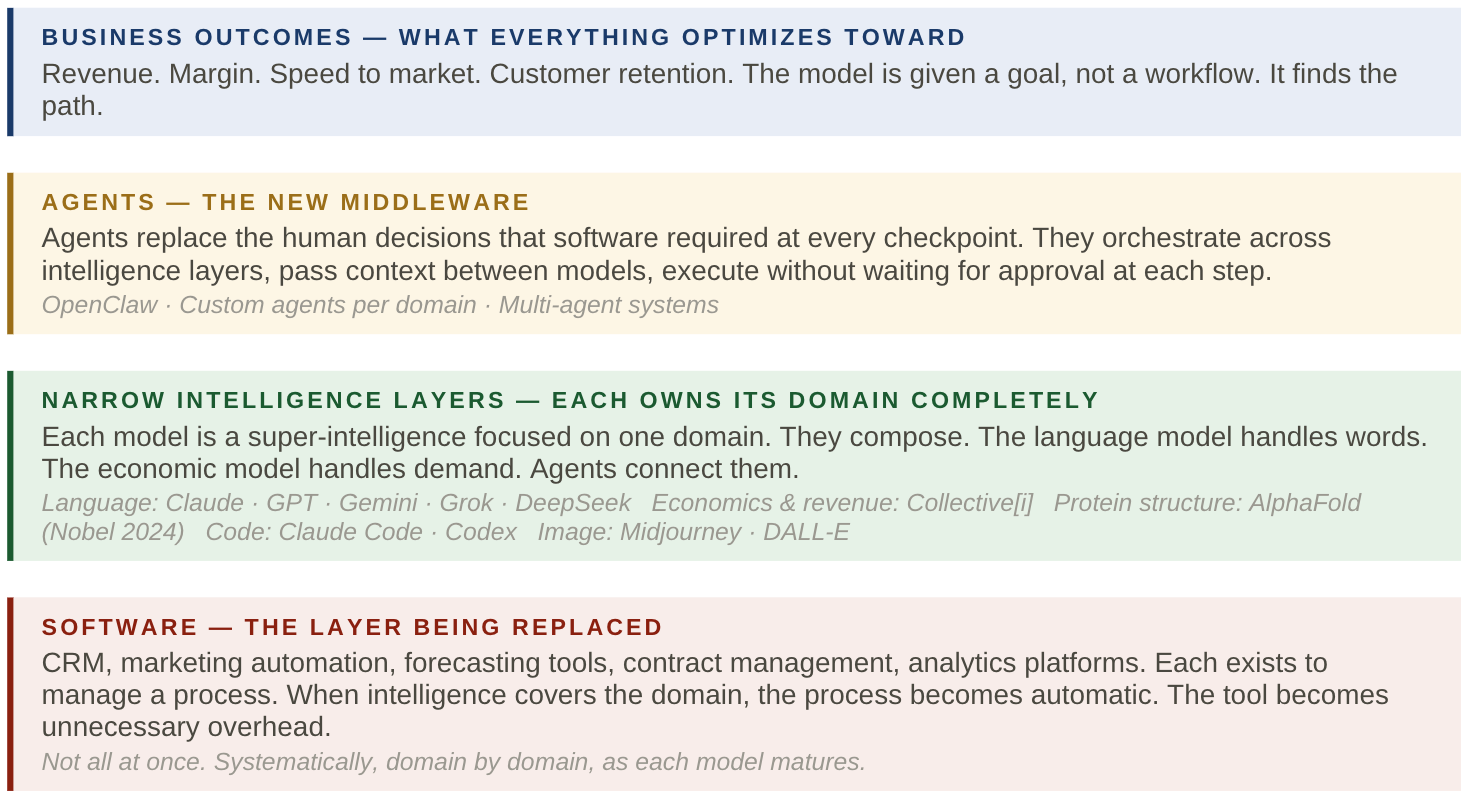

The new stack: intelligence layers, agents as the middleware.

The question is no longer: which software tool do I buy for this workflow? The question is: which models cover the intelligence my domain requires, and how do agents connect them to produce outcomes?

The commercial company using this stack doesn’t forecast revenue by asking its sales team what buyers will do. That’s studying yourself to predict someone else’s behavior. An economic intelligence model does something categorically different: it has watched how this specific buyer, at this specific organization, actually buys. It has seen other sellers deal with them. It has tracked signals across their company, spotted the pattern of how they behave six weeks before a deal closes or dies. This isn’t general market statistics. It’s one-to-one intelligence at network scale. Agents connect that demand signal to inventory positioning, hiring decisions, marketing allocation. Not better forecasting. Different forecasting.

This is a moment for system thinkers, not tinkerers

The companies getting this right are not the ones with the most aggressive AI pilots in isolated departments. They are the ones with leaders who can see the whole system, who understand that replacing a forecasting tool with an AI-wrapped forecasting tool is not transformation, and that the integration problem is not something to solve but something to eliminate by changing the architecture underneath it.

The tinkerer optimizes around the edges. The system thinker asks: if we started over with intelligence as the substrate, what would we build? Not how do we add AI to what we have. What would we build if none of our current workflows were constraints? That question produces a different company.

Here are the warning signs that you have the wrong people making system-level decisions:

01. The AI project owner who buys the AI-branded version of what they already have

"We evaluated six vendors and selected the one that best integrates with our existing workflows."

Integration with existing workflows is not a feature of intelligence. It is evidence that the purchase is a wrapper on the current process, not a replacement for it. The right vendor makes some of your current workflows unnecessary. If the pitch is “works with what you have,” the value is convenience, not transformation.

02. The executive who measures AI against current software benchmarks

"Our AI forecasting is now 15% more accurate than our CRM-based approach."

A 15% improvement on the wrong question is still the wrong question. The benchmark for intelligence is not “better than what we had.” It is “what does this make possible that wasn’t possible before?” A revenue intelligence model that studies buyers at network scale doesn’t just improve your CRM-based forecast; it replaces the premise of that forecast entirely.

03. The IT leader who treats intelligence as an integration project

"We need to connect these models to our existing data infrastructure before we can deploy anything."

Data infrastructure projects take eighteen months. Intelligence moves in weeks. The companies ahead of you right now did not wait for a clean data lake. They deployed on the data they had, learned what the model needed, and improved data quality as the model proved its value.

04. The strategist who builds the AI roadmap around the existing org chart

"Marketing gets the language model. Sales gets the forecasting model. Operations gets the optimization model. Each team owns their AI."

Intelligence doesn’t respect org chart boundaries. The economic model that forecasts demand connects to the marketing model that allocates spend, which connects to the operations model that positions inventory. Agents move context across all three continuously. Organizing intelligence by department recreates the same silo structure that software created.

05. The data leader who says you need clean data before you can use AI

"We need to get our data in order first. Garbage in, garbage out. We can’t deploy intelligence on top of messy data."

This sounds like rigor; it is actually a thirty-year-old excuse for never starting. Companies have been attempting Master Data Management since the 1990s. Almost none of them have clean data. None of them ever will.

Systems of intelligence were built for exactly this environment. They handle labeling, annotation, entity resolution, and data normalization at scale. They are probabilistic by design. They don’t require clean data—they learn to work with the data that exists while improving its quality over time. Start.

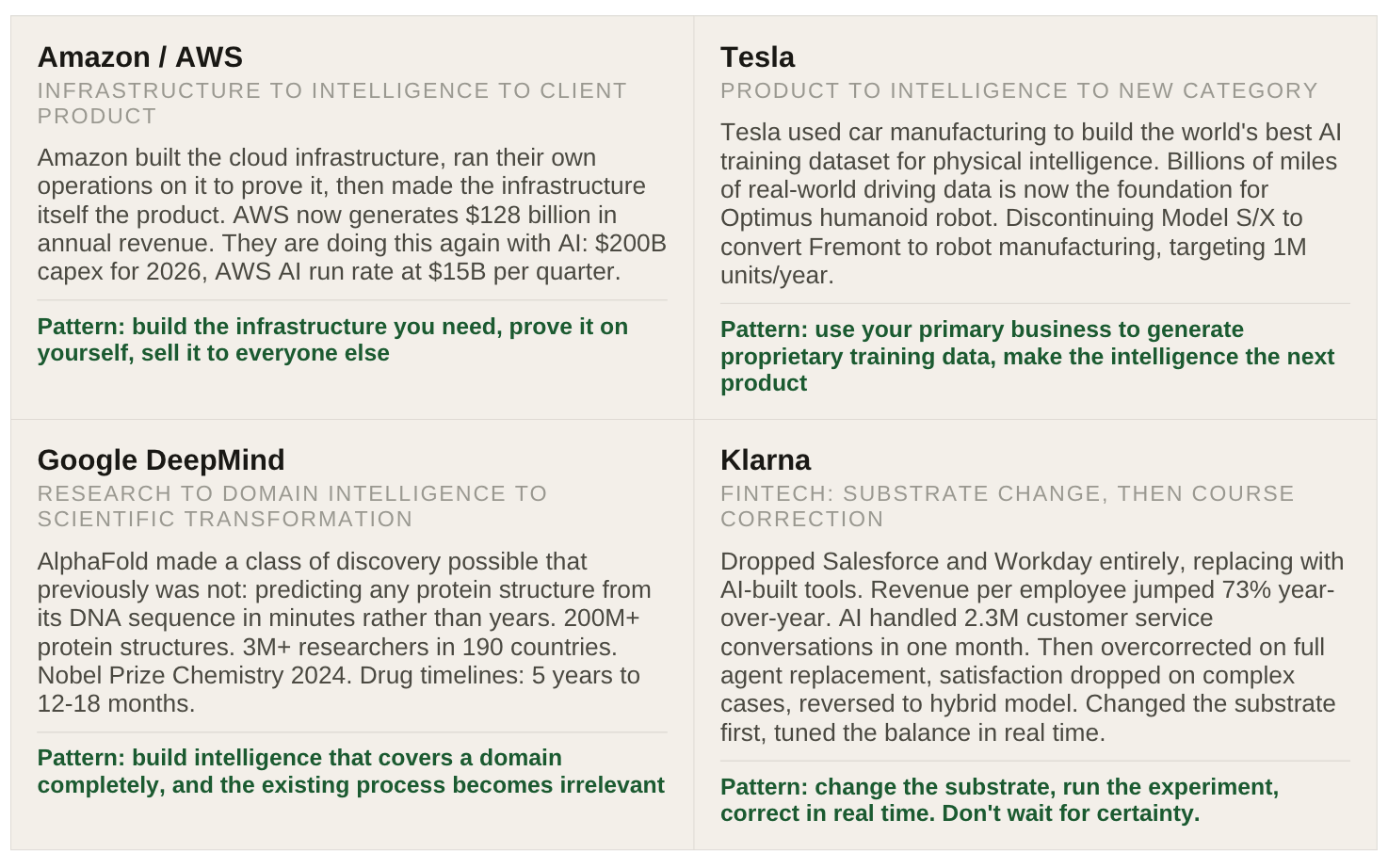

The companies that got it right

The winners from every prior technology transition treated the new substrate as an infrastructure bet and made it early, before the market forced it. They didn’t improve their existing business. They built a new business around it, and then made the intelligence itself the product they sold to clients.

The common thread in the first three: they made an infrastructure bet before the market required it, ran their own operations on it to prove the value, and turned the infrastructure into a product they sold to clients. The intelligence that made the company more efficient became the thing the company went to market with.

That is the CEO question. Not “how do we use AI to improve our operations?” That question produces incrementally more efficient operations. The question is: if the intelligence we’re building to run our business is genuinely powerful, what does it unlock for our clients? The companies with the most compelling answer to that question are the ones building the next decade’s market leaders.

Spend one week with it. Your worldview will change.

Everything above is an argument. Here is the experience that makes the argument unnecessary.

Anthropic built Cowork, a full-featured productivity agent for enterprise knowledge workers, in ten days. Not a prototype. A product shipped to users. Boris Cherny, the creator of Claude Code, confirmed that all of the code was written by Claude Code itself. An AI coding agent built its own sibling product, from nothing to production, in less than two weeks. The team is now shipping 60 to 100 internal releases per day. Roughly 90% of Claude Code’s entire codebase was written by Claude Code.

For context: a traditional enterprise software development lifecycle (requirements gathering, design review, development sprints, QA, staging, deployment) runs six to eighteen months for a feature set of comparable scope. The difference is not that Anthropic has better developers. The development loop has collapsed. When intelligence can write the code it needs, the gap between idea and working product compresses from months to days.

Spend a week running an economic prediction model on your actual pipeline data. Watch it surface risks your CRM never flagged, identify patterns your team never saw, update overnight without a meeting. Something will shift. Not intellectually. Experientially. The feeling is not “this is faster.” It is “the constraint I thought was permanent is gone.”

And then ask yourself: if a competitor, or a new entrant with no legacy stack, is operating in that mode right now, while you are still in sprint planning for the initiative that will start in Q3, how many months before the gap becomes visible to your clients?

Christensen’s Innovator’s Dilemma assumed disruption took years because new entrants had to build distribution, prove value at the low end, then move upmarket. That clock speed assumed the barrier to building was high. Intelligence has removed the barrier. A 25-year-old with Claude Code and a domain insight can build in a weekend what took a team six months. The disruption cycle is not years anymore. It is months. The dilemma is the same. The urgency is completely different.

Parker Harris was right. You should not have to log into Salesforce again. Not because Salesforce is over. Because the browser-based, human-operated, workflow-driven logic that Salesforce represents is over. Intelligence operates on the data directly. Agents handle the decisions. Outcomes are the unit of value, not workflows completed.

Software is over. Intelligence is what comes next. The question is not whether you believe it. It is how fast you act on it.

Real data from companies building on intelligence, not software.

intelligence.com collects real numbers, real results, and real lessons from companies that have made the infrastructure bet and are seeing it compound. Not vendor case studies. Not consultant frameworks. The actual evidence from companies ahead of this curve: what they built, what it replaced, what changed, and what they would do differently.

Intelligence.com

Sources

Market Collapse & Valuation Shift

- SaaS Index Decline: The SaaS index fell 6.5% in 2025, while the S&P 500 rose 17.6%.

- Market Collapse & Valuation Shift

- SaaS Index Decline: The SaaS index fell 6.5% in 2025, while the S&P 500 rose 17.6%.

AI Hyper-Growth vs. Software Stagnation

- Record ARR Scaling: Anthropic scaled from $1B to $30B in ARR in 15 months (April 2026), a milestone that took Salesforce 20 years to achieve.

- OpenAI Momentum: OpenAI tripled its revenue for two consecutive years, reaching a $24B run-rate by April 2026.

- Incumbent Volatility: IBM shares dropped 13.2% in one day—its worst decline since 2000—following news that Claude Code could modernize COBOL.

The "Model Layer" Disruption

- The "Wrapper" Trap: Jasper's revenue collapsed from $120M to $55M in one year after ChatGPT released a superior interface.

- Platform Cannibalization: Lovable reached a $6.6B valuation and $200M ARR within a year, only to face immediate threat when Anthropic leaked a native app-builder integrated directly into Claude.

- Development Loop Collapse: The "Cowork" productivity agent was built in just 10 days, with 90% of its codebase written autonomously by Claude Code.

Infrastructure & Real-World Proof

- Big Tech Capex: Amazon (AWS) hit a $15B quarterly AI run-rate and projected $200B in capex for 2026.

- Tesla’s Pivot: Tesla is converting its Fremont factory to Optimus robot manufacturing with a $20B capex budget.

- Klarna’s Efficiency: After dropping Salesforce and Workday for AI-built tools, Klarna saw a 73% increase in revenue per employee.

- Scientific Transformation: Google DeepMind’s AlphaFold (2024 Nobel Prize) compressed drug discovery timelines from 5 years down to 12–18 months.

- Valuation Repricing: Median SaaS revenue multiples collapsed from an 18x peak in 2021 to roughly 3x by early 2026.

- Salesforce Pivot: On April 15, 2026, Salesforce announced "Headless 360," effectively signaling the end of its traditional browser-based business model in favor of agent-operated infrastructure.