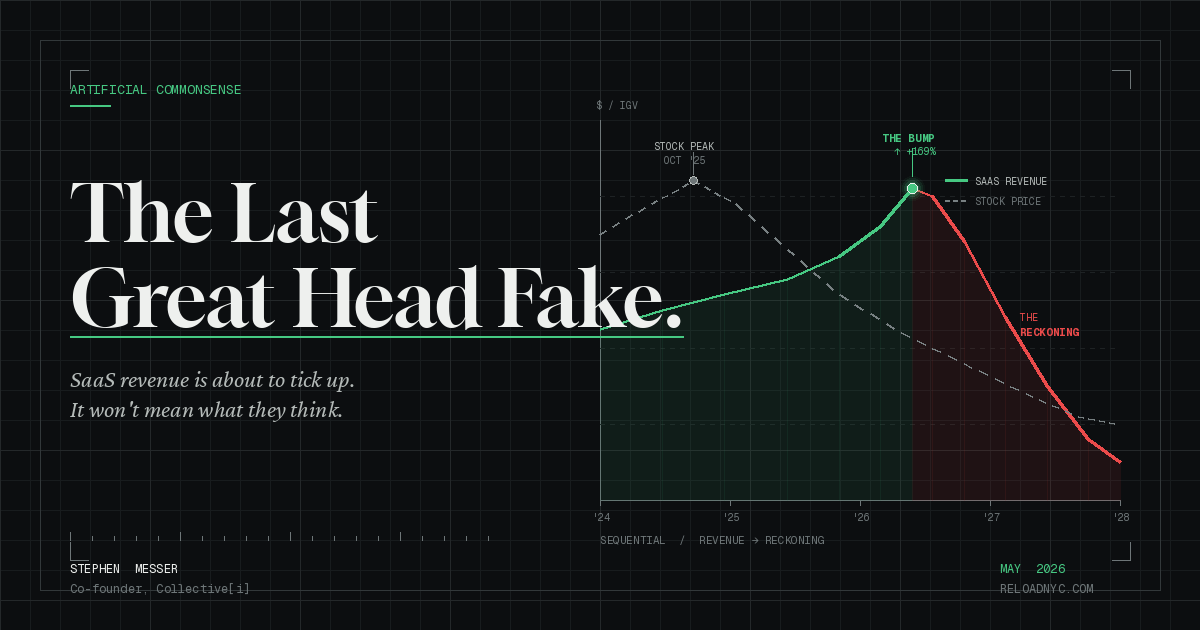

The Last Great Head Fake in Software History.

SaaS revenue is about to tick up. Analysts will call it a recovery. They will be wrong about what it means. The revenue comes first. The reckoning is sequential.

Stephen Messer, Co-founder of Collective[i] and LinkShare (sold to Rakuten for $425M, 1996–2005). Entrepreneur of the Year. Board member, Spire Global (NYSE: SPIR). Building intelligence.com

Goldman Sachs published a piece last week titled "Redefining Software for an Outcome-Driven Future." The IGV software ETF is down 38% from its October 2025 high. Goldman calls this a "large-scale structural transformation" and says incumbents need a fundamental "refounding." They are right about the direction. They are still too conservative about the destination — and too optimistic about the revenue buffer protecting the incumbents while the transition plays out.

Here is the gap Goldman is not fully pricing: SaaS revenue is about to tick up before it falls. The earnings surprises will be real. Analysts will call it a recovery. They will be wrong about what it means. The revenue comes first. The reckoning is sequential.

The Mechanism. Why Revenue Goes Up Before It Goes Down.

Enterprise software contracts run two to three years. The customer is obligated to pay whether or not the AI features are working. The SaaS vendors are running aggressive upsell campaigns on top of that — Agentforce, Now Assist, Breeze Intelligence — selling AI tiers into the existing installed base at premium pricing. A customer paying $500K per year is now being sold a $750K package. They sign it because the MSA is already in place, the IT team knows the platform, and the sales rep is offering a path to looking like they are doing AI without requiring a platform change.

The revenue is not a signal that the AI features are working. It is a signal that the contract signed before anyone knew whether they would work has not yet expired.

Reading the Filings Forensically.

SALESFORCE FY26 Q4 — FEBRUARY 2026

Headline: Agentforce ARR $800M, up 169% YoY. 29,000 deals. Record $11.2B quarter. What the filing says: more than 60% of Agentforce bookings came from existing customer expansion — not new customers choosing Agentforce over AI-native alternatives. Existing customers, already locked into Salesforce MSAs, buying the add-on. The "deals" are upsells into a captive base, not competitive wins.

The metric Salesforce uses to demonstrate adoption: "Agentic Work Units," defined as "decisions made, records updated, or workflows triggered." A record update counts. 2.4 billion AWUs in FY26. The metric was built for the press release, not for evaluating whether the product is creating value proportional to its cost. The one independent proof point in the filing: Agentforce handled 380,000 conversations on help.salesforce.com at 84% resolution — Salesforce, using its own product, on its own support site, for its own customers. The optimal deployment scenario. After one year on the market, that is the independent evidence.

The Einstein precedent is the warning. Einstein launched in 2016 with identical fanfare. Analysis of 500+ verified reviews across Gartner and G2: 67% of enterprise Einstein implementations faced significant adoption challenges within six months, 43% failed to achieve projected ROI within 12 months, 89% of problems traced to data quality. Agentforce has better technology. The enterprise data environment has not changed.

SERVICENOW Q4 FY25 — JANUARY 2026

Headline: Now Assist $600M ACV, doubling YoY. 98% renewal rate. What the transcript reveals: CEO Bill McDermott describing a customer who saved $682 million using ServiceNow: "The customer saved $682 million, and we would be very happy to take a percentage of that savings. But the customer will quickly pull back and say, 'No, no! I like the predictability of the seats.'" The customer has fully quantified the value gap between what they pay and what they receive. They are choosing convenience over economics. That calculation changes.

Also in the guidance, buried in the footnotes: a 150 basis point headwind in Q1 2026 from customers shifting toward hyperscaler-hosted AI services. Customers are beginning to route workflows around ServiceNow's platform entirely. Revenue still growing. The architecture underneath is being bypassed. That is the structural signal, not the ARR headline.

WORKDAY AND HUBSPOT

Workday cut 8.5% of its workforce in February 2025, then another 2% in February 2026 — more than 2,100 employees in twelve months while claiming to be pivoting to AI and returning co-founder Aneel Bhusri as CEO mid-restructuring. HubSpot's Net Revenue Retention fell from 115% to 102% over three years while adding AI features. NRR declining as AI features are being added means customers are not expanding usage at the rate they were before AI was the story. It is a structural signal hiding behind a feature announcement.

WHAT THE FILINGS ACTUALLY SHOW

Why the Revenue Bump Is Shorter Than Goldman Thinks.

Goldman credits the SaaS incumbents — Salesforce, ServiceNow, Workday, SAP, HubSpot — with owning "proprietary data and context" as a moat. Most analysts are treating these companies like a checking account: money flowing in and out, accessible, usable, a live asset. They are actually a safe deposit box. The bank has no access to what's inside. The customer owns the contents. The institution just provides the vault.

The legal reality: none of these vendors own customer data. Their MSAs explicitly exclude it. The practical reality: most enterprise data has already migrated to Snowflake and Databricks. Companies spent the last five years moving data out of application silos to make it accessible to models and analytics tools. The data moat argument assumes enterprise data still lives in the CRM or ERP. Most CFOs moved it somewhere else years ago. What remains in the SaaS system is the workflow architecture — mandatory fields, prescribed processes, standardized objects. That is not an AI asset. It is an AI liability. SaaS systems were designed to standardize human behavior so it could be reported on. AI needs variation to find patterns. The system eliminates variation by design.

There is a second problem. For any business function that influences an external party — a customer, a market, a competitor — using only internal data is studying yourself to predict someone else. Your CRM contains your company's behavior. Your customer exists in a market of millions of interactions you cannot see. The model has too few observations about the thing it is actually trying to predict. This is why Einstein failed, Watson failed, and why so many enterprise AI rollouts on existing SaaS platforms report almost no measurable improvement: it is not a data quality problem, it is a data scope problem.

The companies that solve prediction at scale share one architectural choice: they pool data across the network. Visa sees every payment, not one merchant's transactions. Credit bureaus pool every lender's history because no single lender's loan book is large enough to be predictive. PayPal aggregates signals across hundreds of millions of accounts. Collective[i] was built on this same principle from day one — an economic model trained on the aggregate behavioral patterns of commercial relationships across the entire network, not one company's pipeline. Anyone who understands how AI learns would have arrived at the same architecture. Dashly, a venture-backed startup, applies this model to HR claims fraud in blue-collar industries — a problem invisible to any single employer, visible only in aggregate. These companies keep appearing because there is no other way to build a model that reliably predicts external behavior.

The third problem is the one Goldman underweights most. The shift from on-premise to SaaS — Siebel to Salesforce, Oracle to Workday — was a delivery upgrade. The application logic was roughly the same; moving it to the cloud made it cheaper to maintain and easier to access. AI is not a delivery upgrade. It is a different substrate entirely. The SaaS application layer does not sit alongside AI — it blocks it. A company that learns and improves every day requires intelligence to flow freely across the business, updating models with every interaction, acting on predictions without waiting for a human to enter data into a mandatory field. SaaS cannot do this. It was built for human workflows: rigid, sequential, structured for consistency rather than adaptation. The application layer is not a foundation for AI. It is the wall between where the business is and where AI can take it. COBOL was not a failed technology — it was deeply embedded, functionally adequate, and structurally incompatible with what came next. Banks replaced it. The enterprise application layer is in the same position, with one crucial difference: switching cost is far lower. Going live on an AI-native intelligence layer takes days, not years. What remains is internal alignment — and the market prices that before the alignment happens.

Already visible at the productivity layer: Genspark.ai does not add a copilot to PowerPoint — it replaces the workflow entirely. ChatGPT did not improve Word — it made the document-creation process obsolete for a growing range of tasks. The same displacement is now arriving at the enterprise application layer. Harvey AI is replacing contract review workflows in legal. Lemonade replaced claims workflows in insurance. Rocket Companies replaced the entire mortgage underwriting stack — built Rocket Logic from scratch on Anthropic, OpenAI, and AWS Bedrock with 10 petabytes of proprietary mortgage data, saving 15,000+ underwriter hours per month and closing loans 2.5x faster than the industry average. The CFO on the earnings call: "Head count was down a bit year-over-year. And really, that is the power of AI at work." In every case, the application layer was not updated. It was removed. The 2.5x speed gain was only achievable because the constraint was gone.

The Divergence Is Already in the Public Record.

The companies operating AI-native architectures are not projecting future results. They are disclosing present ones. Microsoft: $500 million in call center savings from AI deployment, generating nearly a third of code for new products, cutting 15,000 employees while growing revenue 13%. JPMorgan: 200,000 employees on its proprietary LLM Suite, $2 billion in annual AI-attributed value in 2025 up from $100 million in 2022, 450 AI use cases in production — built on the intelligence layer, not ServiceNow. Block: 40% workforce reduction, AI handling 90% of code submissions, targeting $2 million gross profit per employee. Klarna: replaced the work of 700 customer service agents with AI, dropped Salesforce and Workday for AI-native alternatives, revenue per employee at $700K versus a $400K industry baseline.

None of these results came from AI add-ons bolted onto SaaS platforms. Every Salesforce and ServiceNow customer reads the same earnings calls. The question "why are we paying $750K per year for a platform when JPMorgan built their own for this workflow" does not require a startup story. It requires the JPMorgan 10-K. When Klarna drops Salesforce and Workday and outperforms its competitors — and the CEO publicly credits the removal — the pressure on those competitors to act mounts with every quarter. At some point the application layer stops being infrastructure to maintain and becomes the constraint everyone can see.

On February 20, 2026, Anthropic launched Claude Code Security. Single-day market reaction: CrowdStrike down 8%, Okta down 9.2%, Cloudflare down 8.1%. The market repriced future earnings the day the threat became credible — not when customers switched. This is how it works. BlackBerry's stock peaked in 2008. Revenue peaked in 2011. The stock correctly priced the decline three years before the revenue moved. The IGV is down 38% while SaaS vendors report record quarters. Both are right. They are sequential.

The Trade. The Specific Call.

Buy the bump. Multi-year enterprise contracts and active AI upsell campaigns guarantee near-term positive earnings surprises. When they arrive, analysts upgrade, multiples re-rate, and the narrative becomes "AI monetization traction is real, the SaaSpocalypse was oversold." That narrative will be right about the revenue and wrong about what it means.

Short the multiple re-rating. Not the revenue — the multiple. When Salesforce re-rates on AI monetization traction while 35% of enterprises have already replaced a SaaS tool with a custom build, JPMorgan is disclosing $2 billion in annual AI value, and Rocket is closing loans 2.5x faster by gutting the application layer — the multiple is wrong. Revenue follows eventually. The multiple leads.

On the Innovator's Dilemma: Nokia had four years from the iPhone's launch to act. They had the technology and the engineers who proposed touchscreen concepts internally. What they lacked was the willingness to cannibalize the profitable existing business. Salesforce knows what a genuinely AI-native CRM looks like. Building it cannibalizes Agentforce. The incumbents who treat the bump as runway to fund a real refounding may survive. The ones who treat it as validation that the current approach is working will miss the window exactly as Nokia did.

The signal to watch is not the vendor's ARR. It is the customers' own filings. Are the largest customers of Salesforce, ServiceNow, and Workday showing AI-like productivity gains, margin expansion, or revenue per employee improvement in their own 10-Ks? If yes, the AI add-ons are working and the bump has more to run. If no, customers are paying for the AI story on the vendor's invoice without getting AI results on their own P&L. That arbitrage closes at renewal — sometimes before. The PE multiplier accelerates this: Anthropic, OpenAI, Google, and Collective[i] are all partnering with major PE firms to deploy AI transformation playbooks across thousands of portfolio companies simultaneously, with 95% of PE funds reporting AI initiatives meeting or exceeding their business case criteria. Each company that shows results becomes a reference that makes the next renewal conversation harder for the incumbent. The velocity compounds faster than most people assume.