Real Disruption

The AI reshaping the world isn't a chatbot. It's in dark factories, drug labs, and autonomous aircraft. That's where the durable value settles.

Stephen Messer, Co-founder of Collective[i] and LinkShare (sold to Rakuten for $425M, 1996–2005). Entrepreneur of the Year. Board member, Spire Global (NYSE: SPIR). Building intelligence.com

The market has made a category error. The hundreds of billions raised to build frontier language models — and the trillions in public market valuation attached to the companies that run them — have conflated one type of AI with AI itself. LLMs and diffusion models are not AI. They are the first AI systems of mass acceptance, built on publicly available human language and images, doing what that data allows: fluent text and image generation. They are extraordinary at what they do. They are also approaching the natural ceiling of what commodity data can produce. The mistake is assuming the ceiling is the sky.

The AI that will actually reshape the global economy is not a better chatbot. It is the AI that makes things — that designs proteins, prints buildings, flies aircraft without pilots, and operates factories with the lights off. This AI has less in common with GPT than a car has with a bicycle. Both are vehicles. The comparison stops there. And most of this AI is happening now — not as a future prospect but as a current market reality — in sectors whose disruption has been hidden from view by the blinding light of the language model fundraising cycle.

What follows is an attempt to describe what is actually happening, where the durable investment value lives, and how to think about it — informed by a decade of building at the intersection of AI and commerce, and by watching the SaaS industry learn the hard way what it costs to misread a technological transition.The known bear case — arguments already in circulation

When we started Collective[i] over a decade ago, we knew neural networks would change the world. The question was where to place our own time and capital. Our conclusion was direct: if you want to compete at the model level, you need access to proprietary data — and a lot of it. Public internet data was going to be available to everyone. The moat, if one existed, had to come from data that could not be replicated.

We focused on a market where network effects and high-value decisions intersected: predicting how businesses make buying decisions. Who will do a deal, when, for how much, for what reason, and how macro factors shift those probabilities day by day. The goal was to make the global economy more predictable. Not as a philosophical ambition — as a product. An AI that runs on proprietary behavioral data, compounding as more participants join the network, in a market where the value created per decision is enormous.

Not every AI investment will have a moat like this. Many won't have the time or resources to build a network. Many are in markets where the proprietary data question remains unsolved. But the underlying framework holds regardless of sector: where does the data come from, who owns it, and does the value created justify the investment required to build on it?

The framing error — and what it costs

The SaaS industry has already paid the tuition for misreading a technological transition. In 2024 and into 2025, the majority of enterprise software companies responded to AI by wrapping their existing products in ChatGPT. "AI-powered" became a product feature rather than a product transformation. The premise was that a large language model as an add-on would be sufficient to protect market position against native AI competitors.

Within a year, the verdict was in. By February 2026, approximately $2 trillion in software market capitalization had been erased in what the financial press called the SaaSpocalypse. The iShares software ETF fell 22% year-to-date. Salesforce lost 26% of its market cap. Atlassian reported its first-ever decline in enterprise seat counts. The structural reason was simple: if AI agents can do the work of ten people, you need ten software seats, not a hundred. The per-seat pricing model that powered two decades of SaaS growth inverts when AI replaces headcount rather than assisting it. A company that spent 2024 wrapping its product in ChatGPT woke up in 2026 to find that ChatGPT's maker was eating its company.

The lesson is not unique to software. It is the canonical pattern of technological disruption: incumbents adopt the new technology as an enhancement to their existing model; new entrants build the new technology as the model itself; the incumbents discover, at speed that surprises them, that enhancement and replacement are different things. The PE firms and institutional investors who own the legacy industries now facing physical AI disruption are looking at a version of the same choice the SaaS companies faced. The ones who understand what is actually happening will use it to drive transformation. The ones who don't will watch a new class of companies replace them at a speed that will feel, in retrospect, breathtaking.

The SaaSpocalypse was not a prediction. By March 2026, it had already happened. Software price-to-sales ratios compressed from 9x to 6x. Enterprise software multiples fell to levels not seen since the mid-2010s. Atlassian reported its first-ever decline in enterprise seat counts. The iShares software ETF (IGV) entered a technical bear market, down 22% year-to-date. Thomson Reuters dropped 15% in a single day. LegalZoom fell nearly 20%.

Thoma Bravo's Orlando Bravo — who has spent 20 years buying and building software companies — said publicly that some companies facing AI disruption are seeing "very warranted" valuation decreases. Gartner now projects that 35% of point-product SaaS tools will be replaced by AI agents by 2030. This happened in approximately one year. The companies that wrapped themselves in ChatGPT in 2024 learned in 2025 that their partner was their predator.

The question every PE owner of a legacy physical industry should be asking: what is my industry's version of this?

The AI that is already reshaping the physical world

The following sectors are not AI hypotheticals. They are current markets where non-LLM AI is already generating measurable economic impact — in some cases at a scale that dwarfs the entire consumer chatbot market. They share a common pattern: the existing players are slow, the processes are old, the data is proprietary, and the value created per transformation is enormous. This is where durable margin lives.

A framework for where durable AI value lives

The sectors above share structural characteristics that generate durable margin. These are not sector-specific observations. They are criteria that generalize. An investor evaluating any AI opportunity should ask whether the following conditions hold:

- Does the AI operate on proprietary data that cannot be replicated?

AlphaFold was trained on decades of crystallographic experimental data. Collective[i] was trained on proprietary network data about business decisions. ICON's construction robots learn from hundreds of completed structures. Dark factory systems train on specific production data from specific facilities. The Commodity Intelligence Problem from Part Two — LLMs trained on public internet data, equally available to every competitor — does not arise when the training data requires years of accumulation and cannot be downloaded.

- Is the value created per decision or per transaction large enough to justify the investment?

Drug discovery: $2 billion and 12.5 years per approved drug, compressed to $600 million and 4 years. Defense: cost-per-effect ratios that favor autonomous systems over crewed aircraft by 10x. Construction: 40% cost reduction on a $400,000 average home. Business intelligence at Collective[i]: predicting the outcome of multi-million-dollar sales decisions. These are markets where the value created per AI intervention is large enough to sustain the investment required to build a proprietary system.

- Does speed change the competitive dynamics in a way that current players cannot match?

This is the most underappreciated dimension. Manufacturing is not being disrupted primarily by lower labor costs — it is being disrupted by speed. Lead times that were acceptable in a world of stable supply chains are catastrophic in a world of geopolitical disruption. A construction process that takes 18 months can be compressed to weeks when design, permitting, and production happen in parallel. Drug development that takes 15 years can be compressed to 4 when AI handles hypothesis generation, structure prediction, and lead optimization simultaneously. Markets should behave at the speed of software. The AI making that possible in physical industries is not an LLM.

- Can a small, focused team with the right approach compete against the largest incumbents?

DeepSeek showed that a small lab could match the largest, most funded AI companies in the world at a fraction of the cost. OpenClaw showed that a single developer could build a product that the industry spent weeks trying to copy. The implication extends beyond software: ultra-small teams, vibe-building at the speed of software, scaling across entire markets in weeks, are disrupting industries whose normal competitive advantage was size and capital. A 3D printing company does not need Boeing's supply chain. A drone company does not need Lockheed Martin's manufacturing base. This is not a future scenario. Anduril is competing for Pentagon contracts that used to belong to primes. Shield AI is building fighter jets. The disruption of established industries by small, focused teams with AI capabilities is happening in real time.

- Are the PE firms and institutional owners of the legacy incumbents building or buying?

Private equity owns enormous portions of the industries most exposed to physical AI disruption: manufacturing, healthcare services, logistics, real estate, defense services. The SaaS lesson suggests that incumbent firms who adopt AI as an enhancement to their existing model will face the same fate as the enterprise software companies that wrapped themselves in ChatGPT. The ones who build for the new paradigm — or acquire the companies already building it — may end up more valuable than their current portfolio structure suggests. This is the PE opportunity and the PE risk, simultaneously.

What this means for how to see the market

The narrative that has consumed investment attention for three years — which model provider will win the LLM race — is the wrong question for the right moment. The LLM race is real. Its financial outcome, as argued in Part Two, is likely to be disappointing relative to valuations. But the more important thing is what the focus on the LLM race has obscured.

The AI in robotics market will be nine times larger than it is today within seven years. The AI drug discovery market will be eight times larger. The AI defense market will be three times larger. These are markets with proprietary data, high value per transaction, and physical-world constraints that commodity language models cannot address. The companies building in them — often with small teams, unconventional approaches, and access to data that incumbents have been sitting on without the tools to use — are competing for something the LLM providers are not: genuinely durable margin.

The SaaS companies that wrapped themselves in ChatGPT in 2024 did not make a bad decision because they were stupid. They made a bad decision because they were looking at the wrong signal. They saw a product — a chatbot — and decided their job was to add it. They did not see the structural reality behind the product: that the same architecture enabling the chatbot was going to dismantle the per-seat business model that funded their growth. The investors and operators now facing AI disruption of physical industries have the same choice. The question is whether they look at the signal or the product.

The attention focused on which chatbot wins has obscured something more important: the AI that will generate durable value is built on proprietary data, applied to high-value physical-world problems, at a speed that eliminates the incumbent's primary competitive advantage. This is happening in robotics, drug discovery, defense, and construction — today, not as a forecast. The companies building here, often with small focused teams, are not competing for the LLM market. They are building something more valuable: moats.

The three-part argument this series has made: LLMs and diffusion models were the first AI of mass acceptance, built on commodity data, already showing commodity economics — bad businesses despite impressive products. The physical-world AI being built on proprietary data, applied to trillion-dollar markets, at speeds incumbents cannot match, is different in every way that matters for long-term investment value. The market's conflation of these two things — treating LLM providers as proxies for all AI — is the most expensive category error in the current investment landscape.

It happened before. In the late 1990s, the market conflated "internet company" with every business that put up a website. The companies that survived and created lasting value — Amazon, Google, Salesforce — were not the ones that were most internet-adjacent. They were the ones that used the internet to do something structurally different in markets with real demand and real margins.

The next version of that is already underway. The dark factory being built in Ohio is not a chatbot. The autonomous fighter jet completing its first flight this fall is not a language model. The drug that just entered Phase III trials, designed by an AI in three years rather than fifteen, was not trained on Reddit.

That is the real disruption. It is happening now.

These ideas deserve more than a comment section.

Connect, push back, or share a perspective at intelligence.com — a professional network built for exactly this kind of exchange.

Sources & data

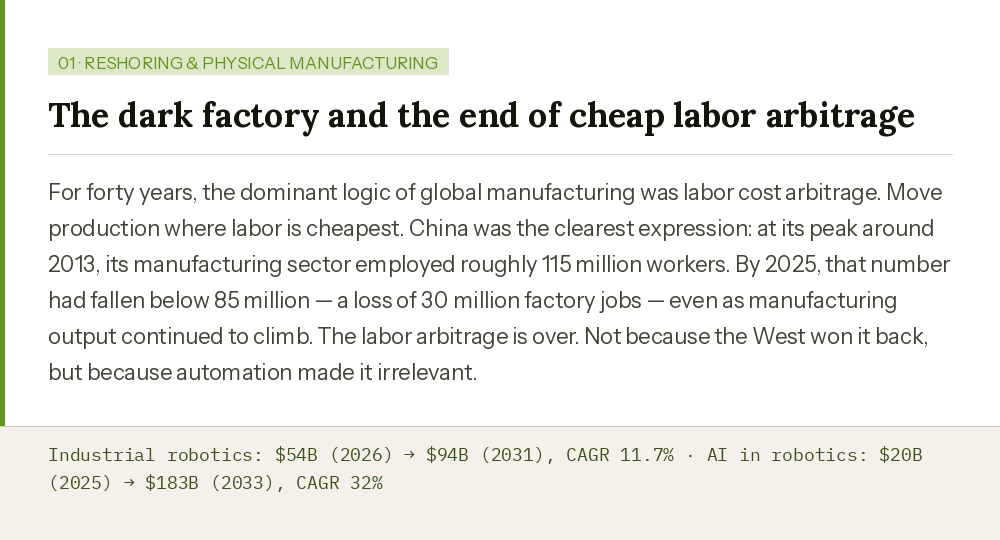

- Industrial robotics market: $54B (2026) → $94B (2031) — Mordor Intelligence, January 2026

- AI in robotics: $20B (2025) → $183B (2033), 32% CAGR — Grand View Research

- 575,000 robot installations in 2025, 700,000+ projected by 2028 — International Federation of Robotics

- China manufacturing employment: 115M peak (2013) → under 85M (2025) — Bloomberg/Metaintro

- Dark factory greenfield segment: 53.7% dominance — Coherent Market Insights

- AlphaFold 3 Nobel Prize in Chemistry 2024 — Nobel Committee; 200M+ protein structures, 43,000+ citations

- Boltz-2 binding affinity prediction: 1,000x faster than physics-based methods — MIT CSAIL/Recursion, June 2025

- 200+ AI-designed drugs in clinical trials; 15–20 entering pivotal trials in 2026; 60% probability of first FDA approval 2026–27 — Axis Intelligence

- Phase II success rates: 65–75% (AI) vs. 30–45% (traditional) — axis-intelligence.com

- AI drug discovery market: $1.9B → $16.5B (2034), CAGR 27% — multiple sources

- mRNA-4157 cancer vaccine: 44% reduction in melanoma recurrence — Phase 2b results

- Former USAF Secretary Kendall flew aboard autonomous F-16, May 2024 — military.com

- Shield AI X-BAT autonomous VTOL fighter unveiled October 2025; first flights expected fall 2026 — military.com

- Ukraine drone production: 4.5M units in 2025 — MIT Technology Review

- EU drone requirement: 3M/year to protect Lithuania in wider conflict — MIT Technology Review

- U.S. DoW FY2026 autonomous systems budget request: $13.4B — PRNewswire

- AI defense market: $9.1B (2025) → $29.5B (2035), CAGR 12.5% — PRNewswire/MarketNewsUpdates

- ICON Titan commercial launch: March 11, 2026; ~$20/sq ft wall systems, 40% cost reduction vs. conventional — 3D Printing Industry, Builder Online

- ICON projected revenue growth: 300%+ in 2026 — Builder Online CEO interview

- ICON completed structures: 245+ — 3D Printing Industry

- LeCun's AMI Labs: $1B raise at $3.5B valuation, March 2026 — CNBC, Let's Data Science

- World Labs: $230M raised; Marble launched November 2025 — TechCrunch

- NVIDIA Cosmos: 2M downloads — NVIDIA Newsroom

- Genie 3: first real-time interactive 3D world model at 24fps — Google DeepMind

- SaaSpocalypse: ~$2T in software market cap erased — multiple financial press

- iShares software ETF (IGV): down 22% YTD 2026

- Atlassian: first-ever decline in enterprise seat counts — SaaStr, February 2026

- Orlando Bravo: AI-driven SaaS valuation decreases "very warranted" — SaaStr, March 2026

- Gartner: 35% of point-product SaaS tools replaced by AI agents by 2030