The Weakest Link

Executives report no AI productivity gains despite record investment. The reason isn't the AI — it's one human-gated function corrupting every signal the rest of the org depends on. Fix it, and everything accelerates.

Stephen Messer, Co-founder of Collective[i] and LinkShare (sold to Rakuten for $425M, 1996–2005). Entrepreneur of the Year. Board member, Spire Global (NYSE: SPIR). Building intelligence.com

In September 2024, a self-taught entrepreneur in Los Angeles named Matthew Gallagher opened a telehealth company with $20,000, a dozen AI tools, and no employees. His first month: 300 customers. His second month: 1,000 more. By the end of 2025 — his first full year in business — Medvi had generated $401 million in revenue. Net profit margin: 16.2%. His only hire: his brother. The New York Times verified the financials. He is now on track for $1.8 billion in 2026. For comparison, his largest competitor runs the same business with over 2,400 employees and a profit margin of 5.5%.

Sam Altman saw this coming. Two years before it happened, he told Reddit co-founder Alexis Ohanian: "In my little group chat with my tech CEO friends, there's a betting pool for the first year that there is a one-person billion-dollar company. Which would have been unimaginable without AI — and now will happen." The bet has been collected. The question every board should now be asking is not whether this was a fluke. It is whether their own industry is next — and whether the team running their revenue function would see it coming before it arrived.

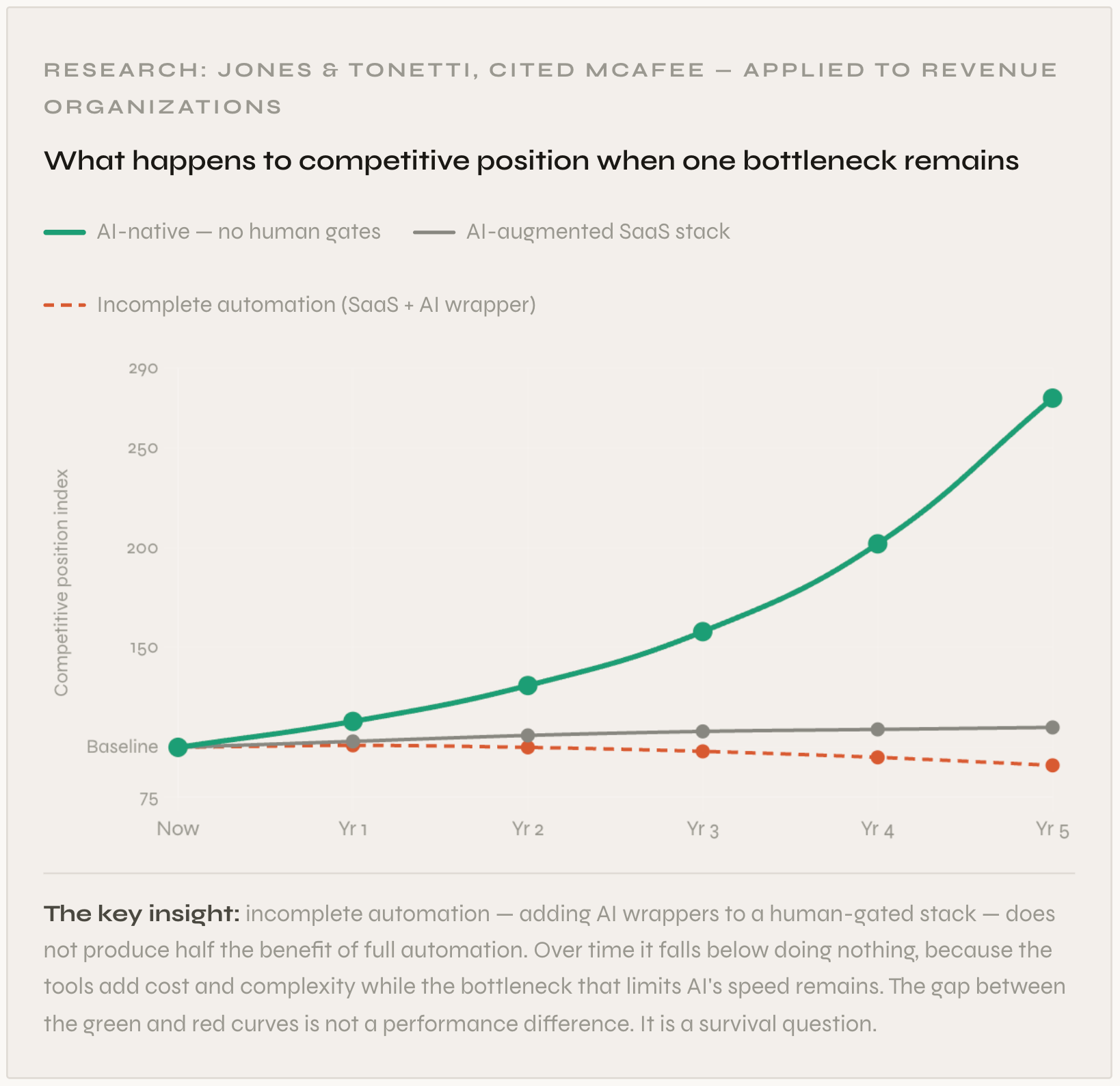

Andrew McAfee published research this week that explains why most of them would not. A survey of CEOs and CFOs across four major economies found that roughly 90% report no measurable productivity impact from their AI investments, despite substantial spending and genuine commitment. A separate paper by economists Jones and Tonetti, which McAfee cited, offers the explanation: the economic benefit of AI does not distribute evenly across the spectrum between "no automation" and "full automation." Organizations that remove every human bottleneck from a process compound their advantage exponentially. Organizations with any human step remaining see the benefit not merely reduced but eventually reversed — falling below where they started, because the cost and complexity of the tools accumulates while the bottleneck that limits AI's speed remains in place.

These two findings — the 90% seeing nothing, the model explaining why — point to the same diagnosis. And the diagnosis points to one function, in virtually every organization, where the problem is most acute, most consequential, and most urgent to fix.

The research — why incomplete automation falls below baseline

Jones and Tonetti's economic model, cited in McAfee's newsletter, runs three scenarios: full automation, incomplete automation, and baseline. The shape of what happens to each over time is the key insight. Full automation compounds — the curve bends upward exponentially as each removed bottleneck accelerates everything connected to it. Baseline continues its gradual improvement. Incomplete automation does something counterintuitive: it eventually falls below baseline, because the cost and complexity of the tools accumulate while the bottleneck that limits the benefit remains in place.

The following is that dynamic compressed to a business-relevant timeline. The x-axis is five years. The curves are the same three scenarios applied to competitive position:

This is the chart that explains why 90% of executives see no AI productivity impact. They are in the middle curve or the bottom one. They have added AI to processes that still require humans at critical steps. The AI waits at those steps. The benefit does not compound. The cost grows. The gap between them and the rare organization that has removed the bottleneck entirely widens with every passing quarter.

The revenue function — and why it is the one that matters most

Every function in an organization is downstream of the revenue signal. Finance builds its models on the revenue forecast. HR plans headcount against pipeline. Fulfillment stages inventory against predicted deal close. Marketing allocates budget toward segments where demand is strongest. When the revenue signal is accurate, live, and uninterrupted, every downstream function operates on reality. When it is delayed, corrupted, and human-gated, every downstream function makes decisions based on last week's distorted picture of the world.

This is why the revenue function is not merely one bottleneck among many. It is the upstream source of the signal every other AI investment depends on. A company can deploy AI across finance, supply chain, marketing, and HR — and if the revenue signal those systems wait for is a weekly opinion assembled from partial CRM data adjusted twice for political reasons, every AI investment downstream is running on bad input. Garbage in. The chain is only as fast as its slowest link. In most organizations, the revenue function is that link — and it has been deliberately engineered to run on a weekly human cycle.

Consider what happens when a macro event occurs — a conflict, a trade shift, a competitor move. In an organization with a human-gated revenue function: some reps hear about it, someone flags it in the weekly pipeline call, the forecast adjusts next week, and downstream functions respond next month.

In an organization where the revenue signal is live and uninterrupted: the network detects the shift in buyer behavior within hours. The signal updates. HR agents adjust hiring plans. Fulfillment reroutes product. Sellers receive updated deal priorities. The CFO's view of the quarter adjusts. Marketing reallocates. All of this before your competitor's weekly pipeline call has started.

No amount of AI investment in HR, finance, or marketing can compensate for receiving the revenue signal a week late. Cost savings cannot offset lost revenue. The math has never worked that way and never will.

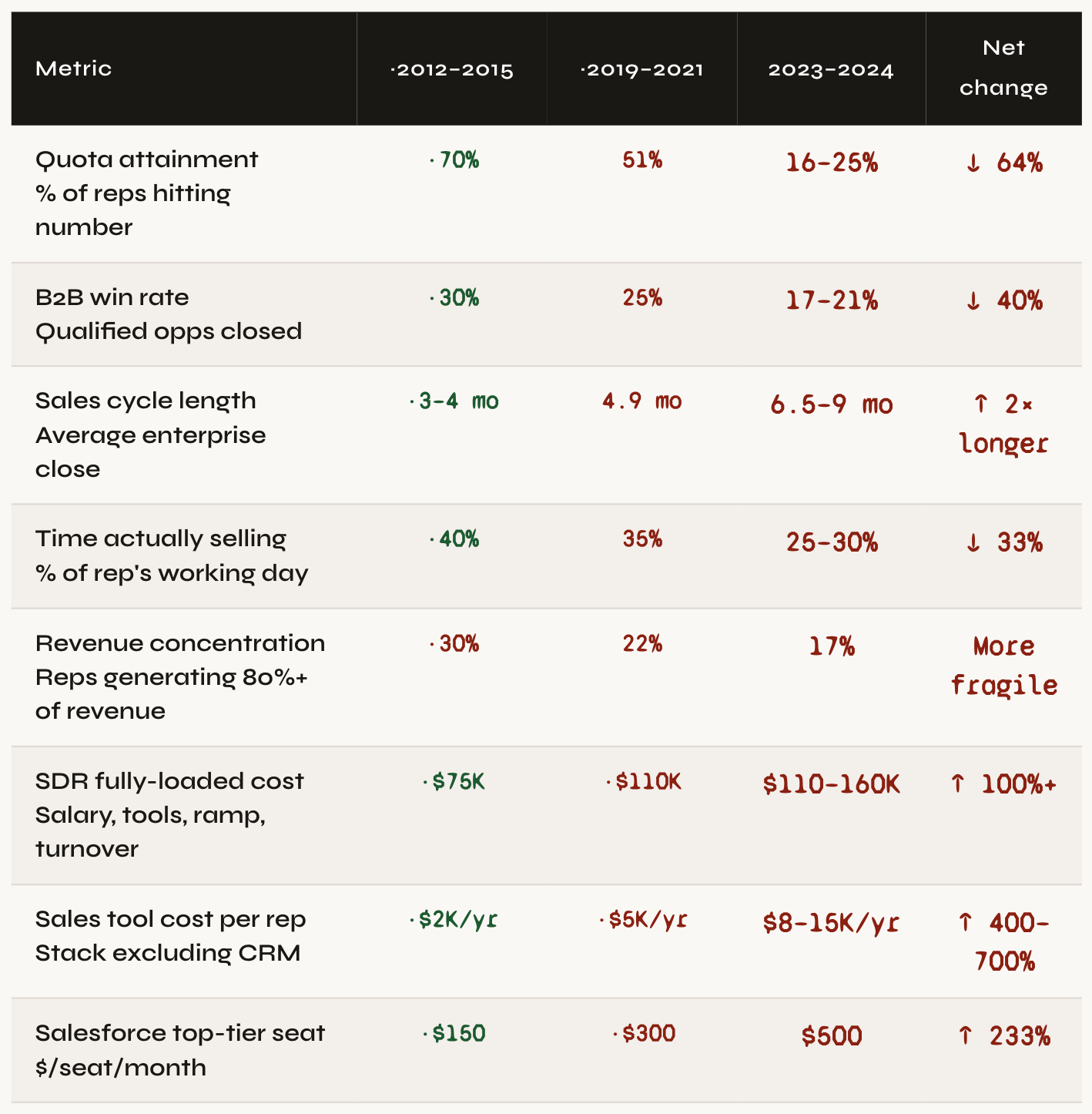

What fifteen years of adding tools actually produced

The modern enterprise revenue function did not arrive at its current state through negligence. It arrived through the reasonable accumulation of reasonable tools, each solving a real problem, each requiring humans to bridge the gap to the next one. CRM to capture activity — but reps enter it. Call recording to analyze conversations — but managers review it. Pipeline tools to flag risk — but someone has to act on the alert. Engagement platforms to sequence outreach — but a human approves each send. Forecasting tools to surface trends — but the weekly call is still where the number gets set.

Every tool was good. The architecture was wrong. And the metrics document fifteen years of that architectural mistake with painful clarity:

This table is the incomplete automation curve made concrete. Every tool investment added cost. Every tool added human steps. Every human step consumed time that was not spent selling, not spent on buyers, not spent on the work that produces revenue. The metrics declined in perfect proportion to the growth of the stack.

The industry's answer to each metric decline was another tool. The next tool added another gate. The gate consumed more time. The metric declined further. This is not irony — it is the predictable, documented outcome of incomplete automation applied to the most upstream function in the organization.

Who the stack was built for — and who it was not

Here is the part of this story that almost nobody says out loud: the sales stack was not built for sellers. It was built for managers.

CRM was designed as a database for leadership to have pipeline visibility — not as a tool that helps a rep understand a buyer. Call recording was built so managers could review conversations — not so reps could arrive at the next meeting more prepared. Pipeline forecasting was built to give the CFO a number — not to help a seller understand which deal deserves their attention today. Forecast calls, pipeline reviews, status updates, QBRs — every one of these is internal. Every one consumes rep time. Not one of them is a conversation with a buyer.

The result: reps spend 72% of their working week on things that have nothing to do with the person they are supposed to be serving. Data entry. Internal meetings. Research that should be automated. Reporting that serves management, not the buyer. According to Salesforce's own research, the average rep dedicates just 28% of their week to actual selling. The Forrester Activity Study puts it even lower in some segments. The three-quarters of the day that disappears goes to feeding the management system — not to understanding the customer.

This would be merely inefficient if buyers had not simultaneously moved in exactly the opposite direction. In the same period that reps' time with buyers fell to a quarter of their day, buyer expectations for those interactions rose sharply:

71% of B2B buyers expect personalized interactions and report frustration when they don't receive them (McKinsey). They want to deal with a seller who understands their specific business, their specific problem, their specific moment — not someone running a generic pitch.

77% of B2B buyers say they won't consider a purchase if the content and approach isn't personalized to their needs (MarketingProfs). The rep who arrives with a standard deck is not getting a second meeting.

70% of the purchasing process is complete before a buyer talks to a seller (6sense). The buyer already knows the category. They are evaluating whether this specific seller understands their world well enough to be worth talking to. The rep who has spent the morning on a forecast call is arriving to that conversation behind.

61% of buyers now prefer a rep-free experience entirely (SalesHive). This is not a preference for no human contact. It is a verdict on what human contact has delivered: generic, unprepared, self-serving. The rep who knows the buyer's world, their timing, their actual problem — that rep is irreplaceable. The rep who doesn't is optional.

This is the gap that fifteen years of stack-building opened. The tools optimized for management reporting. The buyers moved toward demanding deep, individualized understanding. The rep caught between them had less time for buyers and less information about each specific buyer — at the exact moment when buyers required more of both.

This is why AI applied to the revenue function is not about automating sales. It is not about replacing sellers. It is about doing something the stack never could: giving sellers back the time and the intelligence they need to actually sell. The internal work — the data entry, the forecast calls, the pipeline reviews, the research, the briefing preparation — none of that requires human judgment. All of it requires human time. Remove it, and the seller's entire working day becomes available for the only thing that actually requires them: the buyer.

A seller operating with Collective[i]'s intelligence behind them arrives at every interaction already knowing what the buyer cares about at this specific moment, which deal signals indicate urgency or stall, which relationship in the network changes the outcome, and what the optimal approach is for this specific person at this specific stage. They are not doing that research. The network did it. They are not maintaining that forecast. The system updated it. They are not in an internal pipeline review. The agents handled it. They are with the buyer — prepared, specific, and focused on what only a human can do: build trust, exercise judgment, close the deal.

Why the SaaSpocalypse is the signal — and what the insiders are telling you

In February 2026, the enterprise software sector suffered what traders at Jefferies immediately christened the "SaaSpocalypse." The iShares Tech-Software ETF entered a technical bear market, falling more than 20% year-to-date. Salesforce lost roughly 30-40% of its value over twelve months despite beating earnings — its guidance of 10-11% forward growth was treated as a confession. ServiceNow fell 34% year-to-date, 50% from its highs. Workday dropped 40%+. HubSpot, Atlassian, Docusign, Adobe — all crushed in what SaaStr's Jason Lemkin called "pure get me out selling." The narrative from Wall Street: if AI agents can do the work of ten sales reps, you don't need ten software seats. You need one.

That narrative is right as far as it goes. But the damage to public market software companies is only the visible part of the story. The sharper signal is in the private market — where the insiders who built and funded the revenue software stack are quietly making moves that tell you everything you need to know about where this is going.

The conversation intelligence leader — the company whose core product was recording and analyzing sales calls — raised at a $7.25 billion valuation in 2021. In early 2026, secondary transactions are pricing its shares at approximately $4.5 billion: a 38% markdown from peak, even as its revenue tripled. The founder says an IPO is "interesting but not the most important thing." Translation: they cannot go public at 2021 multiples, and every investor who funded them at those multiples knows it. Meanwhile, call recording and conversation analysis are now standard features in every major CRM platform. The moat that justified a $7 billion valuation evaporated. Too big to sell, can't IPO, competing against free.

Two pipeline-and-engagement platforms — both PE-backed, both stalled at the same revenue ceiling — were forced to merge in December 2025 to create scale. The combined entity has four overlapping products, three redundant capabilities, a new CEO with no founding context at either company, and product unification described in their own documentation as "coming years" away. The founders who built both companies had already left — one in 2023, one in 2024. This is not a product vision materializing. It is two investors trying to bundle enough recurring revenue to find a viable exit.

The sales engagement pioneer — valued at $4.4 billion in 2021 — conducted four rounds of layoffs between 2023 and 2024, cutting roughly a third of its workforce. Its founder and CEO departed in September 2024. The company has not raised new capital in over three years.

None of this is rumor. It is the documented behavior of investors who know these companies best. When insiders mark down valuations, force consolidations to cut costs, and install professional managers to manage the exit, they are telling you something. If the tools your revenue team depends on are in survival mode, this is not a time to wait for renewal. It is a time to find a replacement.

The deeper signal, which the SaaSpocalypse confirmed and the private market underscores: the SaaS stack architecture and full AI benefit are structurally incompatible. You cannot retrofit one into the other. The companies that tried to add AI wrappers to human-gated workflows are being valued accordingly. The companies built from the start on a different architecture are the ones the market is looking for.

Why this is not ChatGPT for sales — and why that distinction matters

Every executive who has experimented with ChatGPT or Claude for commercial decisions has noticed the same thing: the output sounds authoritative and reads fluently, and it is frequently wrong about the specific thing that matters. Which buyer is actually moving? Which deal will close? Which relationship changes the outcome? What does the shift in a buyer's engagement last week signal about next month? Language models produce words. Commercial decisions require something trained on a fundamentally different signal.

Large language models are the most powerful word engines ever built. Ask OpenAI or Anthropic to draft a proposal, write an email, or summarize a document — they are extraordinary. That is exactly what they are optimized for: language that sounds right.

Commercial decisions require something different. Who will buy, and when? Which deal will close and which will quietly die? Which relationship changes the outcome? What does a buyer's behavior last Tuesday signal about their likelihood to close next month? These are not language questions. They cannot be answered by a model trained on the internet, no matter how fluent. A language model can write you a plausible-sounding answer. Plausibility and accuracy are not the same thing — and in economic decisions, the difference costs revenue.

Think of the distinction this way: Bloomberg Terminal is to financial markets what Collective[i] is to commercial markets. A live feed of what is actually happening, with intelligence trained on real transactions, real relationships, real outcomes — not on text descriptions of them. You would not ask ChatGPT whether to buy a stock. You should not ask it whether your deal will close.

Collective[i] is the intelligence layer for economic decisions — the same category of advance for commercial outcomes that Bloomberg represented for financial ones. Not made up. Not a pilot. Working, in production, at Fortune 500 companies, today. The results are in the numbers above.

What the alternative actually is

The alternative to the stack is not a better stack. It is a fundamentally different kind of system — one that replaces the need for a stack entirely. Not a collection of tools that require humans to bridge their gaps. One intelligence. One continuous signal. Every function of the revenue process handled by the same brain, learning from the same network, acting on the same real-time view of the world.

When we started Collective[i] a decade ago we made the foundational choice: we would not build another tool. We would build the alternative to tools. That meant building on a network — not on your CRM, not on your deals, not on your history — but on the actual behavior of commercial relationships across the global economy. Deal by deal, buyer by buyer, relationship by relationship. Every interaction that flows through the network teaches the system something about how decisions get made, when buyers move, what changes the outcome of a deal, which signals matter.

The result is a neural network that knows more than any team could. It has seen more negotiations, more relationship patterns, more macro shifts, more competitive dynamics than any combination of tools could surface. And it applies that knowledge continuously, automatically, to every deal in every rep's pipeline — not when asked, not on a weekly schedule, but the moment the signal changes.

Pipeline intelligence: Every deal reviewed continuously, automatically. Risk identified when it signals in the data — not after a weekly review. Optimal paths surfaced for each specific deal with each specific buyer at this specific moment. No rep has to figure this out. The brain does.

Relationship intelligence: The network maps who knows whom across the entire economy. It surfaces the connection that changes a deal's outcome before the rep has thought to look — not from your CRM, from the full graph of commercial relationships that no individual could see.

Buyer intelligence: Before every conversation, the rep knows exactly what this specific buyer cares about, where they are in their decision, what has changed since the last interaction, and what approach works for this person at this moment. Not generic research. Personalized signal from everything the network knows about this buyer and deals like this one.

Conversational intelligence: Not recordings waiting for a manager to review later. Signal from every interaction flowing into the brain in real time, updating the deal model, adjusting the optimal approach before the next conversation happens.

Autonomous agents: Handling everything internal — forecast updates, pipeline reviews, briefing preparation, CRM maintenance, activity capture. All of it runs without the rep. Everything that was consuming 70% of the working day and producing management reports instead of buyer conversations. Gone.

No team to operate it. API access to systems you already own. The brain handles the internal. The seller focuses on the buyer. This is what selling was always supposed to be.

This is what the architecture change produces — in numbers from organizations that have made it:

The 13% win rate improvement in Q1 is not a training outcome. It is not a process improvement. It is what happens when sellers stop spending 70% of their day feeding a management system and start spending it on buyers who now expect exactly the kind of personalized, informed, specific engagement that the stack was preventing them from delivering. The brain handles the internal. The seller handles the buyer. That is the only allocation that produces the results buyers demand and markets reward.

The economics — even the worst case compels action

Here is what the transition looks like from a pure cost standpoint for a representative 50-person enterprise revenue team:

The worst case — where performance improvements take longer to materialize — is still a compelling cost consolidation. The best case — which customer data supports as the realistic case — is that the architecture change reverses fifteen years of metric decline in the first year. The logic is symmetric: if adding human gates to the chain produced the decline, removing them produces the recovery.

The leadership question boards have not yet asked — but will

There is a pattern to how technological transitions punish leadership teams that miss them. When advertising moved from newspapers to the internet, companies that did not have a digitally fluent CMO by 2005 were at a measurable disadvantage by 2010. The job title did not change. The required skills did. CMOs who could not think in data, attribution, and algorithmic targeting were replaced — not because they were bad marketers but because the terrain of marketing had become unrecognizable to them. Gartner now predicts that by 2027, a lack of AI literacy will be a top-three reason CMOs are replaced at large enterprises. Only 15% of CEOs currently believe their CMO is AI-savvy.

The same reckoning is arriving for the revenue function — and it is arriving faster, because the evidence is already in the results.

A CRO who has spent the last five years optimizing a human-gated stack — more SDRs, better sequences, tighter pipeline review discipline, incremental AI features bolted onto existing tools — has built expertise in a methodology that the data shows is declining along every metric simultaneously. They are not failing. They are succeeding brilliantly at something that is no longer the right game. The question is not whether they are a good leader. It is whether they are the right leader for the next five years. BCG published a formal series in 2025 on what "AI-first" leadership looks like at each C-suite level — CMO, CPO, CTO. The series exists because boards are asking the question.

When ad spend shifted from the New York Times to Google, boards asked: do we have a digital CMO? When manufacturing shifted to software-driven production, boards asked: do we have a technology-native COO? The pattern holds. Every major platform transition surfaces the same question at the leadership level.

The current transition — from human-gated revenue processes to AI-native intelligence systems — is no different. The question is simply later to arrive in the boardroom than the technology itself. Does the company have AI-first leaders at each level of the revenue function? Not leaders who have added AI to their existing playbook. Leaders who understand that the playbook itself is what has to change.

Matthew Gallagher built a $400 million company in one year, alone, using AI tools. His competitors had thousands of employees, sophisticated revenue stacks, and experienced leadership teams. He beat them on margin by a factor of three. He did not have a better CRO. He had a different architecture. The board that understands this distinction now has time to act on it. The one that figures it out after a competitor has made the same move will be asking different questions.

The insight that unlocks all of this is simple. It does not require a management consultant or a new framework. It requires noticing that two things happened simultaneously over the last fifteen years and treating them as one story rather than two. Tool investment in revenue functions went up every year. Every performance metric in those same functions went down every year. The tools were sold as the solution. They were, in fact, the cause — because each one added a human step, and each human step slowed the chain that AI needs to run at full speed.

The 90% of executives who report no AI productivity impact are not at the start of an AI journey. They are in the middle of an architectural mistake. And the architectural mistake has a name: the revenue function, still running on weekly human cycles, still feeding corrupted data downstream, still built to serve managers rather than buyers — at exactly the moment when buyers expect more, and competitors are building organizations that deliver it automatically.

Matthew Gallagher figured this out with $20,000 and a dozen AI tools. The question his story raises is not whether AI can outperform a traditional revenue organization. It already has. The question is how much time remains before a competitor in your specific market has the same realization — and whether the leadership team now running your revenue function will see it before or after they arrive.

Find the weakest link. It is not a technology problem. It is an architecture decision. And unlike most strategic decisions, this one has a clear before and after — documented, verified, already happening in companies that made it.

No team to operate it. API access to systems you already own. The brain handles the internal. The seller handles the buyer. This is what the architecture change looks like in practice.

The results are documented. The transition is happening. The only variable is timing — yours, and your competitor's. collectivei.com

Sources & data

- Matthew Gallagher / Medvi: $401M revenue (2025), $1.8B projected (2026), 16.2% net margin, two employees — NYT (Erin Griffith, April 2, 2026), verified financials

- Sam Altman one-person unicorn prediction: interview with Alexis Ohanian — Fortune/PYMNTS, August 2025; "would have been unimaginable without AI and now will happen"

- 90% of executives report no measurable AI productivity impact: survey of US, UK, Germany, Australia CEOs/CFOs, November 2025–January 2026 — cited in McAfee, "Yes, AI Should Be an OKR," The Geek Way newsletter

- Jones & Tonetti incomplete automation model — McAfee newsletter, April 3, 2026

- Reps spend 28–30% of their week actually selling — Salesforce State of Sales 2024; 50% of rep time on admin — Gartner

- 72% of rep time spent on non-selling tasks — Forrester Activity Study, 3,031 reps

- CRM built for managers, not reps: 37% of reps admit fabricating CRM data — DevRev/AskElephant, 2026

- 71% of B2B buyers expect personalized interactions — McKinsey

- 77% of buyers won't consider a purchase without personalization — MarketingProfs

- 82% of decision-makers agree buyers expect personalized experiences — Forrester, 2024

- 70% of purchasing decisions complete before engaging a seller — 6sense, 2024

- 61% of buyers prefer a rep-free experience — SalesHive/Landbase

- By 2027, AI literacy will be a top-3 reason CMOs are replaced at large enterprises; only 15% of CEOs believe their CMO is AI-savvy — Gartner (survey of 402 senior marketing leaders, August–October 2025, published February 23, 2026)

- BCG AI-first leadership series — bcg.com, 2025–2026

- SaaSpocalypse: iShares IGV ETF −22–25% YTD 2026; Salesforce −30–40% over twelve months; ServiceNow −34% YTD, −50% from highs; Workday −40%+ — SaaStr/Jason Lemkin, February 2026; FinancialContent, February–April 2026

- Conversation intelligence leader: $7.25B valuation (2021) → $4.5B secondary (2026) — TechCrunch; Calcalist/Sacra

- Pipeline-engagement platform merger — Business Wire, December 3, 2025

- Sales engagement platform layoffs and founder departure — GeekWire, 2023–2024

- Quota attainment, win rate, cycle length, SDR cost, tool cost — Salesforce State of Sales (multiple editions), Bridge Group, Ebsta, HubSpot, Gartner, SaaStr

- Collective[i] customer results — Collective[i] internal data

- "Waze for sales" — The Wall Street Journal